PCCA Cotton Market Weekly 28-Mar-2025

Posted : March 31, 2025

March 28, 2025

Cotton prices rose this week but remained within a tight trading range. Export shipments remained strong, yet mill demand stayed soft. The technical trends outlook remains weak. However, with a major USDA report set for release next week regarding the 2025 crop year, will it help drive a positive shift in next year’s prices, or will challenges persist? Get QuickTake’s read on the week’s events in five minutes.

Cotton prices found support and ended the week higher on strong volume.

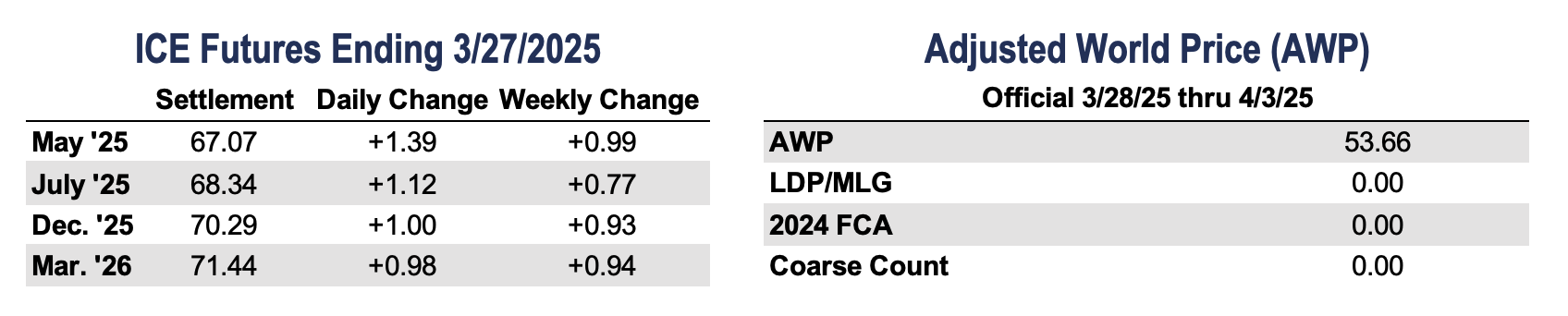

- The May contract settled at 67.07 cents per pound, gaining 99 points for the week. Thursday’s settlement marked the contract’s highest close in nearly two weeks.

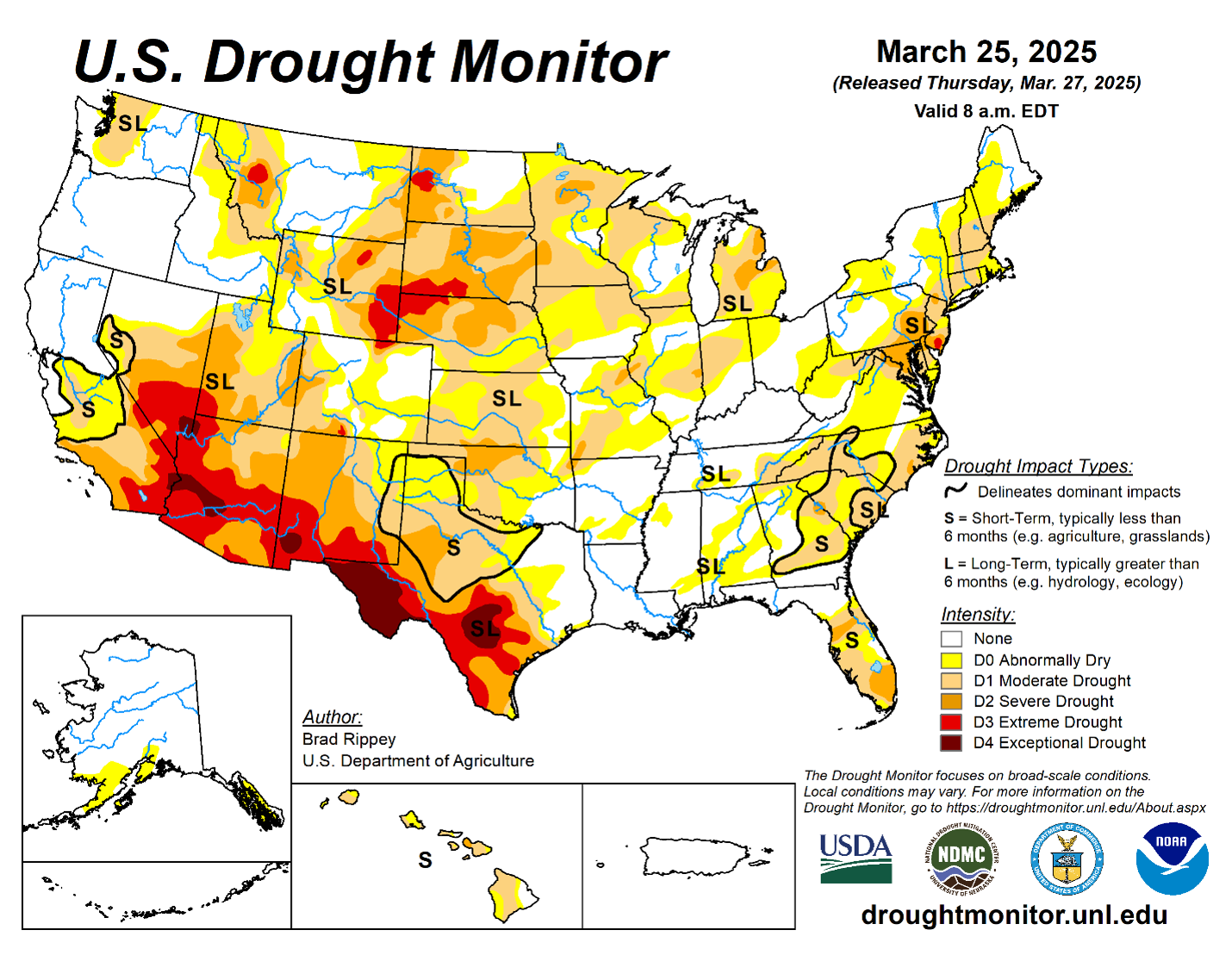

- Cotton prices rebounded this week, though the market remains uncertain due to ongoing tariff concerns, as noted in the weekly Export Sales Report. Prices stayed rangebound between 65 and 67 cents. Thursday’s triple-digit rally had no single cause, but short-covering likely contributed, alongside excessive rainfall in Australia and a drought monitor showing widespread drought in the Southwest. The market faces significant risk from speculators’ large short positions, tariff tensions, and uncertainty over global crop sizes.

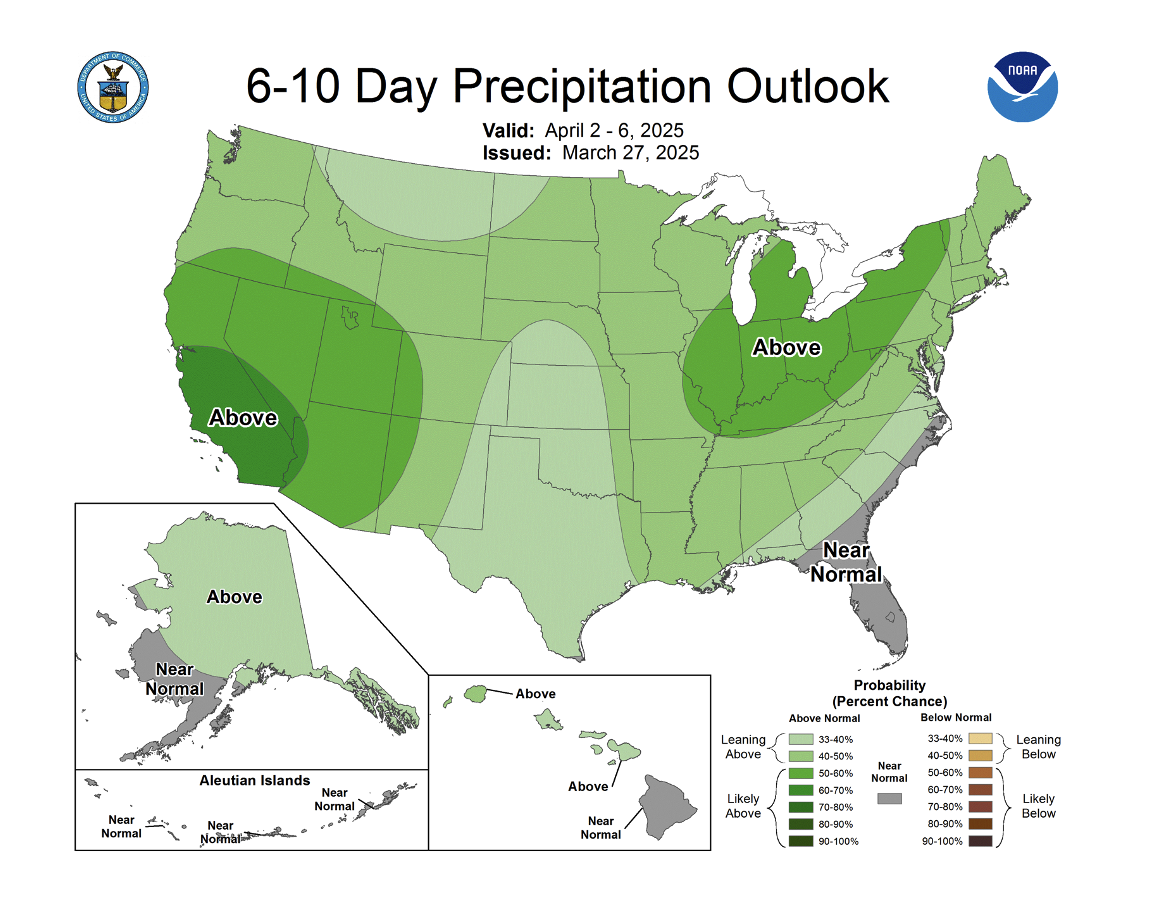

- South Texas received beneficial rainfall, although some areas in the Lower Valley experienced excessive amounts, reaching up to 14 inches. Overall, the rain should help with planting and provide much-needed soil moisture to support crop emergence where planting has already taken place. However, the planting pace across the area varies significantly this year due to a lack of moisture at the start of the planting season.

- Trading volumes were substantial, and open interest rose by 9,504 contracts, totaling 284,585. Certificated stocks remained unchanged at 14,488 bales.

Stock markets were mixed but ultimately ended lower as newly imposed tariffs and ongoing concerns about trade tensions fueled market volatility. Publicly traded companies in the consumer discretionary sector, such as Ralph Lauren and Ross stores, have taken a beating (down more than 9% in the last month), which is not good news for commodities like cotton.

- The Conference Board reported that the consumer confidence index fell to 92.9, dropping seven points—a larger decline than expected. The Expectation Index indicates that short-term forward-looking expectations for the economy, including income, business, and labor conditions, are at their lowest level in 12 years. However, recent reports show that economic growth has remained solid in the past few weeks.

- The Fed’s preferred inflation measure, the February Personal Consumption Expenditure (PCE), rose 0.8% month-over-month. Consumer spending also slowed, increasing only 0.1% month-over-month, compared to the expected 0.3%. Overall, it was a mixed bag of data—indicating that consumers may be pulling back on spending, which suggests the Fed will likely remain in a holding pattern with interest rates.

- The April 2 tariff deadline is quickly approaching. This week, however, a 25% tariff was imposed on global automotive imports to the U.S. Stock markets were trending upward before the announcement but quickly reversed course afterward.

- Next week’s impending tariffs appear to be aimed at trading partners with whom the U.S. has a significant trade imbalance. The U.S. Trade Representative to China is set to release a report on April 1, assessing whether China has upheld its commitments under the Phase 1 trade agreement. Reports suggest that China is prepared to retaliate against any tariffs the U.S. imposes. However, given the unpredictable nature of tariff developments, this could change by the time they take effect.

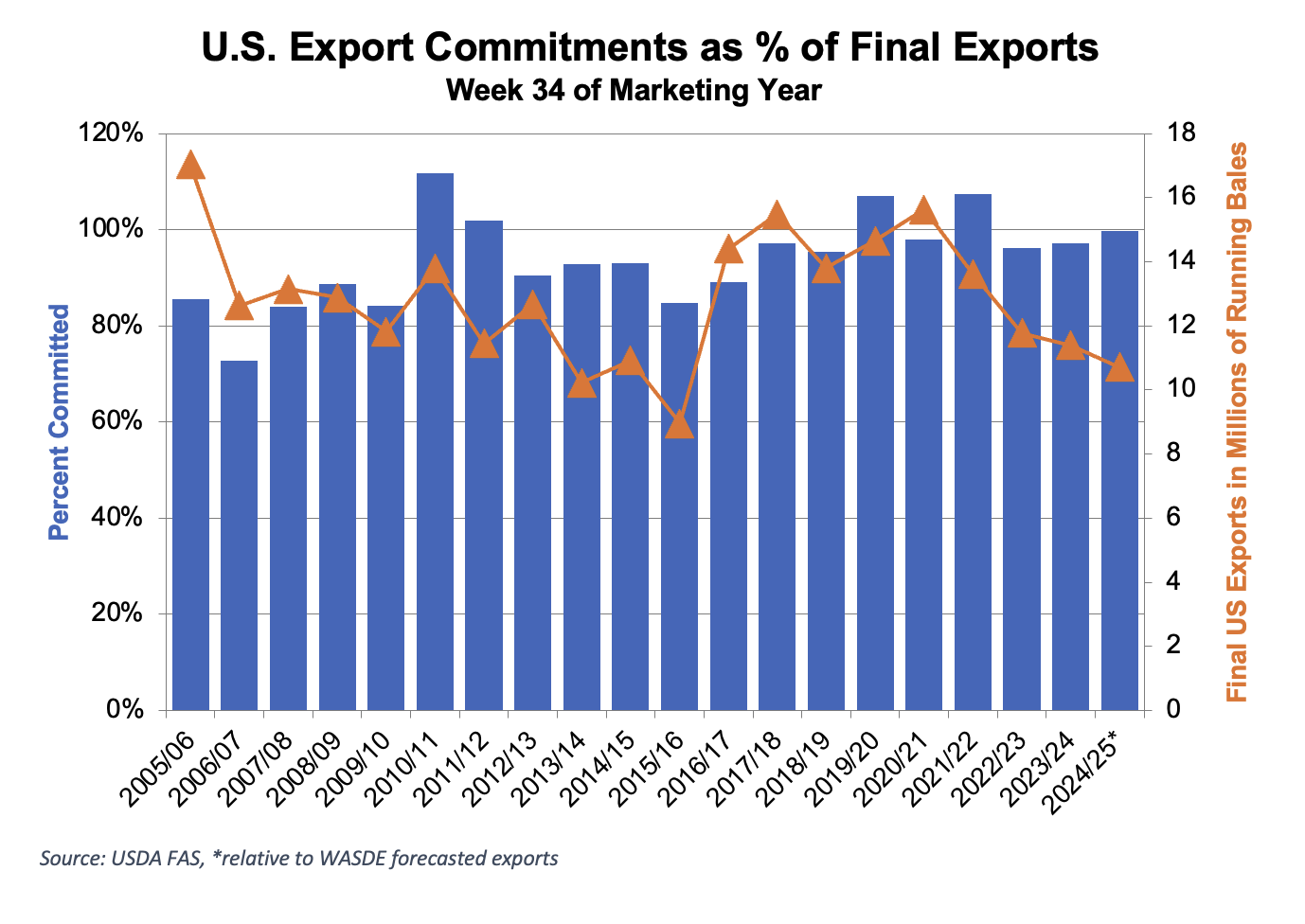

U.S. export sales continue to lag, but shipments remain strong.

- For the 2024/25 marketing year, U.S. merchants sold 84,400 Upland bales and shipped 393,400. While export market sales were disappointing, it was not entirely unanticipated. Most countries in the market for U.S. cotton have purchased the same amount, if not more, than usual. But China, which used about a third of all cotton, has been absent from the market. There were some cancellations from China, which were not entirely unexpected given the implications of tariffs.

- Pima sales and shipments remain strong. Merchants booked 19,900 bales and shipped 11,900, putting Pima sales and shipments above the pace needed to reach USDA’s estimates.

The Week Ahead

- Next week is a big week for the cotton market. USDA will release the Prospective Plantings report on Monday, March 31, at 11:00 AM CST. This report is pivotal because its estimate will be used to forecast production for the May and June WASDE reports. The average analyst estimate for the report is 9.9 million acres, which is higher than the National Cotton Council’s estimate of 9.6 million acres and USDA’s estimate from the Ag Outlook Forum of 10 million acres.

- There are many economic headline risks in the coming days. The March unemployment number will be released on April 4, and tariff policy and impacts will continue to be monitored.

Announcements

- Enrollment for the U.S. Cotton Trust Protocol is now open through April 30, 2025. Currently enrolled growers will need to renew their membership to continue their involvement in the program. Click here to see a list of enrollment dates.

- New Grower Enrollment for Better Cotton will be open March 3-May 30.

- For assistance or questions about enrolling in these programs, contact PCCA at 806-763-8011.

The Seam

As of Thursday afternoon, grower offers totaled 109,987 bales. During the week, 18,587 bales traded on the G2B platform at an average price of 62.84 cents per lb. The average loan was 50.77, which resulted in a premium of 12.07 cents per lb. over the loan.