Unpredictable. Interesting. Pick your adjective to describe the data flow this week, which includes multiple inflation readings and personal income. We’re also watching developments in Congress on government funding, as current funding is set to expire on September 30. At this point, the chances of a government shutdown appear high, though we can’t rule out a short-term deal at the last minute. Both the House and Senate are on recess this week, so it’s just leadership working behind the scenes. Last week, the House passed a bill to extend funding, but it was blocked in the Senate, where a vote is expected to be forced next week. Government shutdowns are never good for cotton. Most of the time, the shutdowns occur during harvest, which means the loan is unavailable.

For cotton, the focus remains on crop progress, weather, and export opportunities, along with broader market forces and how USDA will address the pressures weighing on farm income.

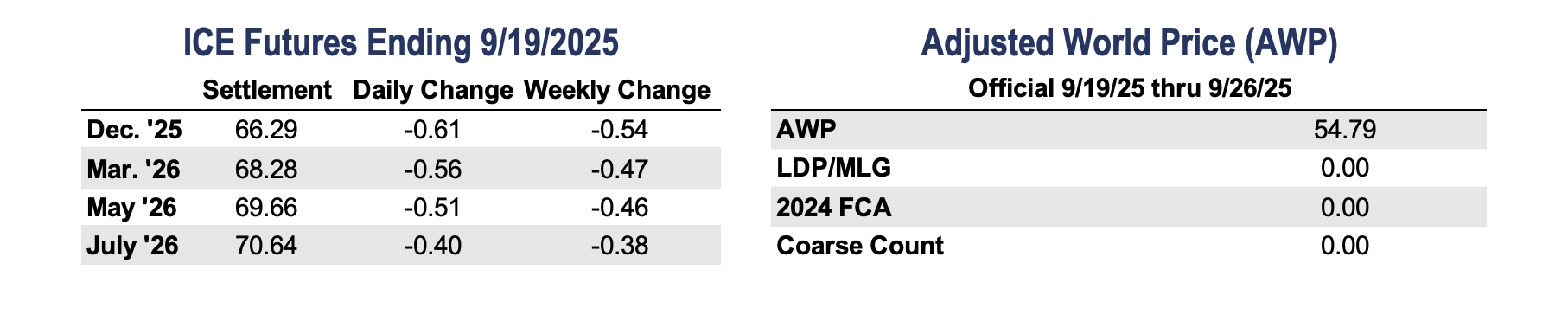

Market Recap

Cotton futures tried pushing through the 100-day moving average but couldn’t hold it, leaving December back in a choppy, range-bound trade even after briefly touching new weekly highs. December futures gave back any early-week gains, finishing the week 54 points lower at 66.29 cents per pound.

Export chatter picked up, with a bit more U.S. cotton in the mix, though most buyers remain hand-to-mouth given lingering macro and trade uncertainty. The latest CFTC Cotton On-Call report highlighted the trend, showing yet another record gap between unfixed sales and purchases. On the macro side, a 25-bp Fed cut, stronger retail sales, and a softer dollar gave the market a mid-week boost. Still, futures couldn’t hang on to the gains and slid back toward the middle of the recent range.

Speculators trimmed short positions but are still carrying a record net short for 73 straight weeks. Daily volumes were more active, yet the technical picture remains flat even after testing key signals, leaving the market vulnerable to sharp moves. Open interest climbed 1,446 contracts to 257,429, while certificated stocks held at 15,474 bales.

Economic and Policy Outlook

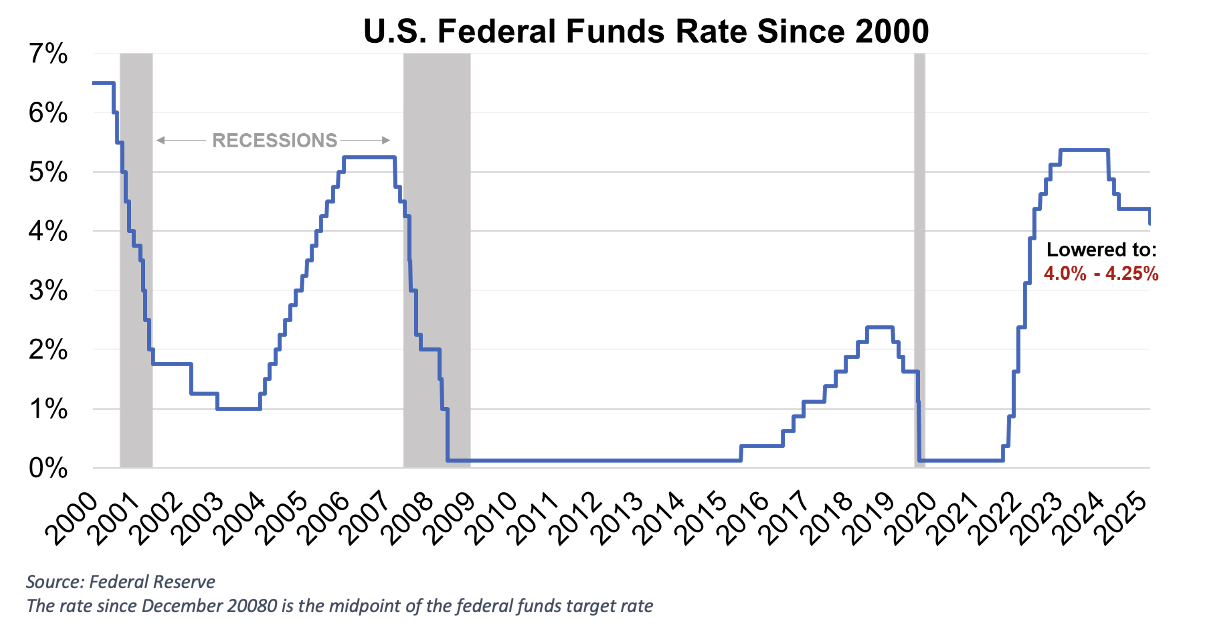

The Fed delivered the expected 25-bp cut, lowering rates to 4.00–4.25% and signaling two more moves could follow before year-end. The dollar eased on the news, while August retail sales surprised to the upside, rising 0.6% month-over-month and 5.0% year-over-year, with clothing sales up 1.0% on the month and more than 8% higher on the year. Stronger consumer data and a softer dollar provided a friendlier backdrop for commodities mid-week, even as broader uncertainty limited gains. For cotton, a weaker dollar supports U.S. competitiveness abroad, but signals of higher demand are just not there yet. U.S. and Chinese officials met again on bilateral trade, though little tangible progress was made for commodities (it appears that TikTok got most of the attention from negotiators).

Weather and Crop Watch

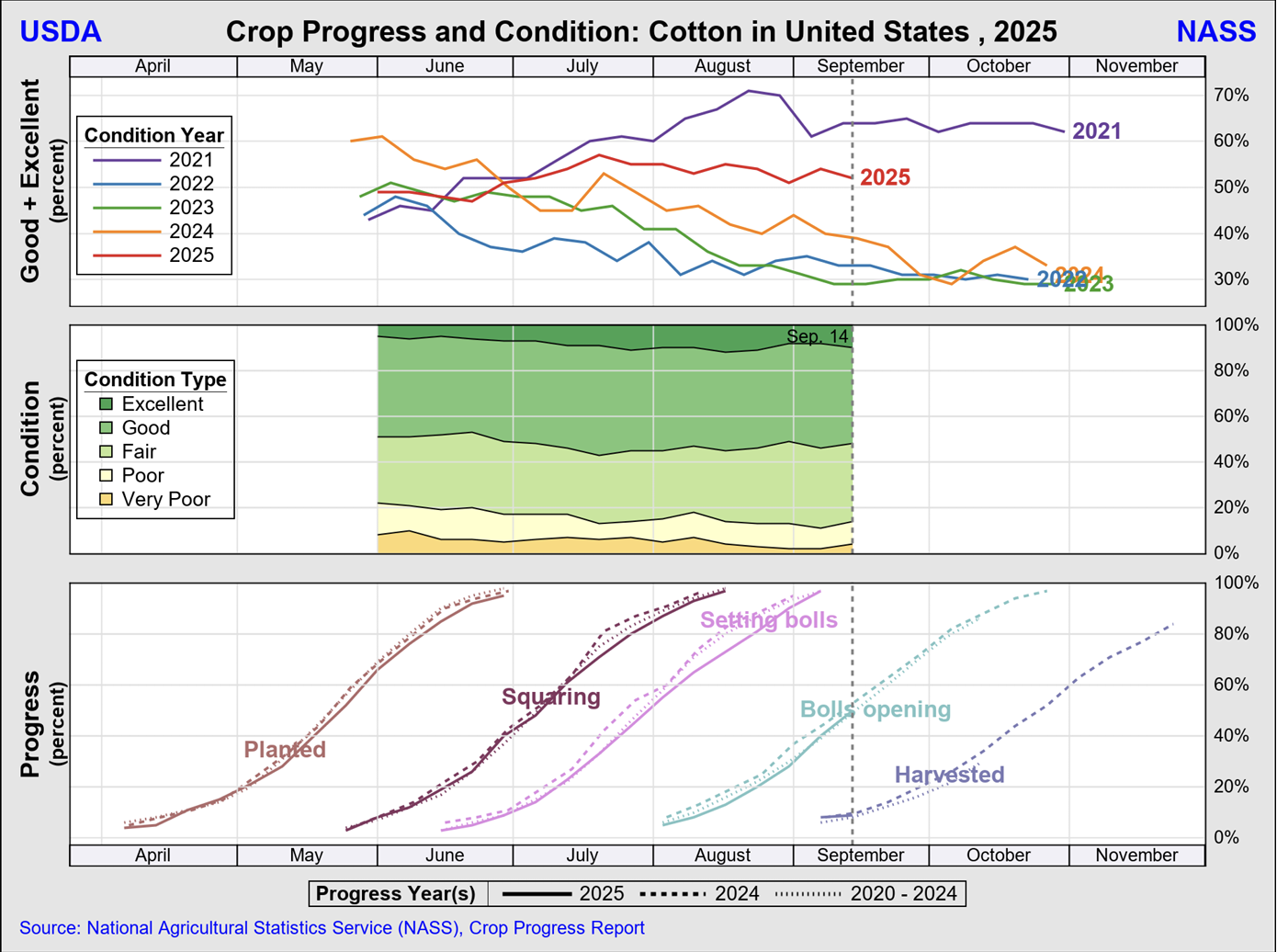

Southwest crop conditions remain mostly favorable, with Oklahoma slipping to 67% good to excellent, Texas down marginally at 47%, and Kansas down to 64%. Boll opening has reached 46% in Texas, 38% in Oklahoma, and 20% in Kansas. Harvest is moving quickly in South Texas, with more than 80% complete, bringing the statewide harvest to 21%.

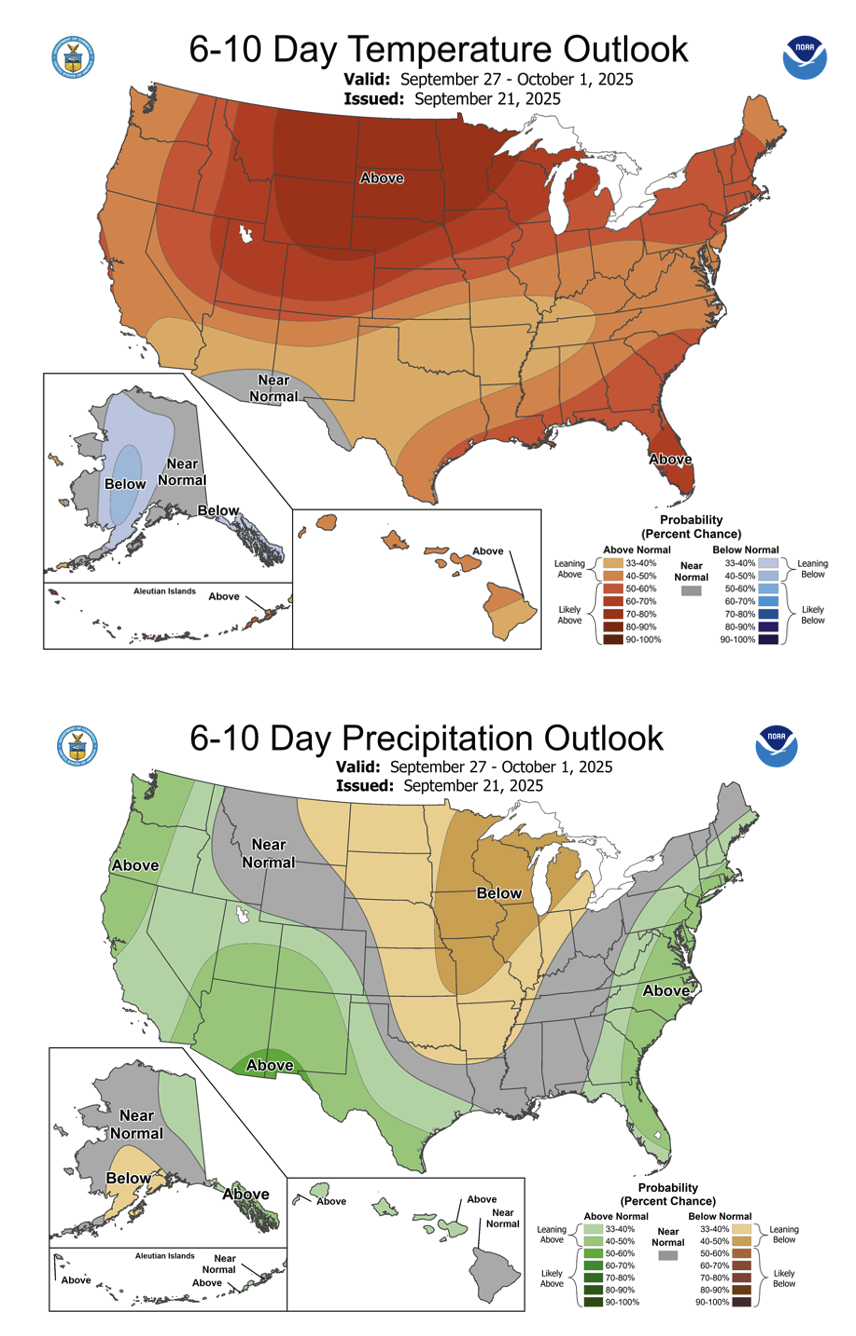

Weekend rains brought up to two inches in southwestern Oklahoma and lighter totals across the Panhandle, West Texas, and South Texas. Scattered showers early to midweek could potentially discolor open cotton, but a drier stretch into early October should improve fiber quality and support maturation. South Texas may see up to three-quarters of an inch midweek, though conditions otherwise favor harvest. Temperatures will run seasonable to warm, with midweek cooling.

Export Trends

Export sales improved this week, with net Upland commitments of 186,100 bales, up from the prior week and above the recent 4-week average. Vietnam led with 77,000 bales, followed by India, Malaysia, Turkey, and Pakistan. Forward sales for 2026/27 totaled 19,000 bales, all for Vietnam.

Shipments slowed to 120,500 bales, down from both the prior week and seasonal norms, reflecting ongoing competition from other growths and limited U.S. availability.

For Pima, new sales rose to 5,200 bales, led by India, Pakistan, and Thailand, while shipments fell to 2,400 bales, primarily to India. Sales remain ahead of pace, though shipment volumes have eased in recent weeks.

The Seam

As of Friday afternoon, grower offers totaled 22,070 bales. There were 5,775 bales that traded on the G2B platform that received an average price of 64.82 cents per pound. The average loan for these bales was 56.02, bringing the average premium received to 8.80 cents per pound.

Latest News

U.S. EXPORT SALES

For Week Ending 05-Feb-2026

2025-2026

Net Upland Sales 2,31,000

Upland Shipments 1,88,600

Ne