Markets are moving with an odd mix of confidence and caution, but the clock runs out on funding on Tuesday, and uncertainty is building. President Trump is set to meet with the four congressional leaders later this afternoon in a last-ditch effort to strike a deal (none of the parties seem to have much incentive now). If Congress can’t reach an agreement, the release of Friday’s jobs report could be pushed back, leaving investors to rely on job openings and other labor indicators to gauge the economy. Worse yet, several vital USDA programs, such as the marketing assistance loan, will be shelved until the impasse is resolved. The dollar has eased from last week’s highs, while stocks continue to trade firm into quarter-end.

For cotton, the main themes remain crop progress, weather, and export opportunities. Hurricane worries have eased with Humberto now steering clear of land, taking that risk off the table. The bigger concern is whether a shutdown disrupts USDA programs at a critical time, which could include next week’s supply and demand update.

Market Recap

December futures were slightly higher last week, adding 11 points to settle at 66.40 cents per pound after trading in a tight range. Cotton prices remain stuck in their months-long narrow range, with the technical outlook still flat to bearish. A close above key resistance levels could spark some upside, but rallies have been consistently met with selling pressure.

ICE cotton futures held in a tight range as prices continue to search for direction, with recent sessions marked by some of the smallest daily moves in years. Macro pressures from a stronger dollar and shifting interest rate expectations have added weight, while U.S. assistance programs and trade policy updates have provided only limited market spark. An imbalance in cotton on-call positions remains and could become a source of pressure for the market down the road. Overall, cotton remains supported near the 66-cent area, but traders still await clearer signals to drive the next move.

Speculators added to their short positions and have now carried a record net short for 74 consecutive weeks. Trading volumes were active last week, with open interest rising 14,500 contracts to 271,929. Certificated stocks held steady at 15,474 bales.

Economic and Policy Outlook

August Personal Consumption Expenditures (PCE) rose 0.3% on the month and 2.7% year-over-year, with core up 0.2% and 2.9%, keeping the Fed cautious as inflation proves sticky. U.S. personal income increased 0.4%, while spending climbed 0.6%, showing resilience even as savings shrink and wages cool. Oil hit seven-week highs on supply concerns, and the dollar strengthened, making U.S. cotton less competitive abroad at a time when export demand is already soft.

Tariffs and market disruptions have been tough across the board. President Trump pledged that tariff revenues would be directed to farmers as a bridge until his trade strategy begins to deliver longer-term benefits. He emphasized that money collected from tariffs would be distributed back to producers to help offset weak export demand, volatile prices, and uncertainty in global trade flows. However, no details were announced about how the money would reach the country. Most experts believe that the same Congress, which hasn’t funded the government, would have to approve any aid package to farmers.

The Emergency Commodity Assistance Program (ECAP) payment factor was recently raised from 85% to 99%, essentially paying out all the money approved by Congress for eligible losses. In addition, USDA has delivered $2 billion through the Emergency Livestock Relief Program (ELRP) and more than $5.5 billion through Stage 1 of the Supplemental Disaster Relief Program, with Stage 2 details expected in October.

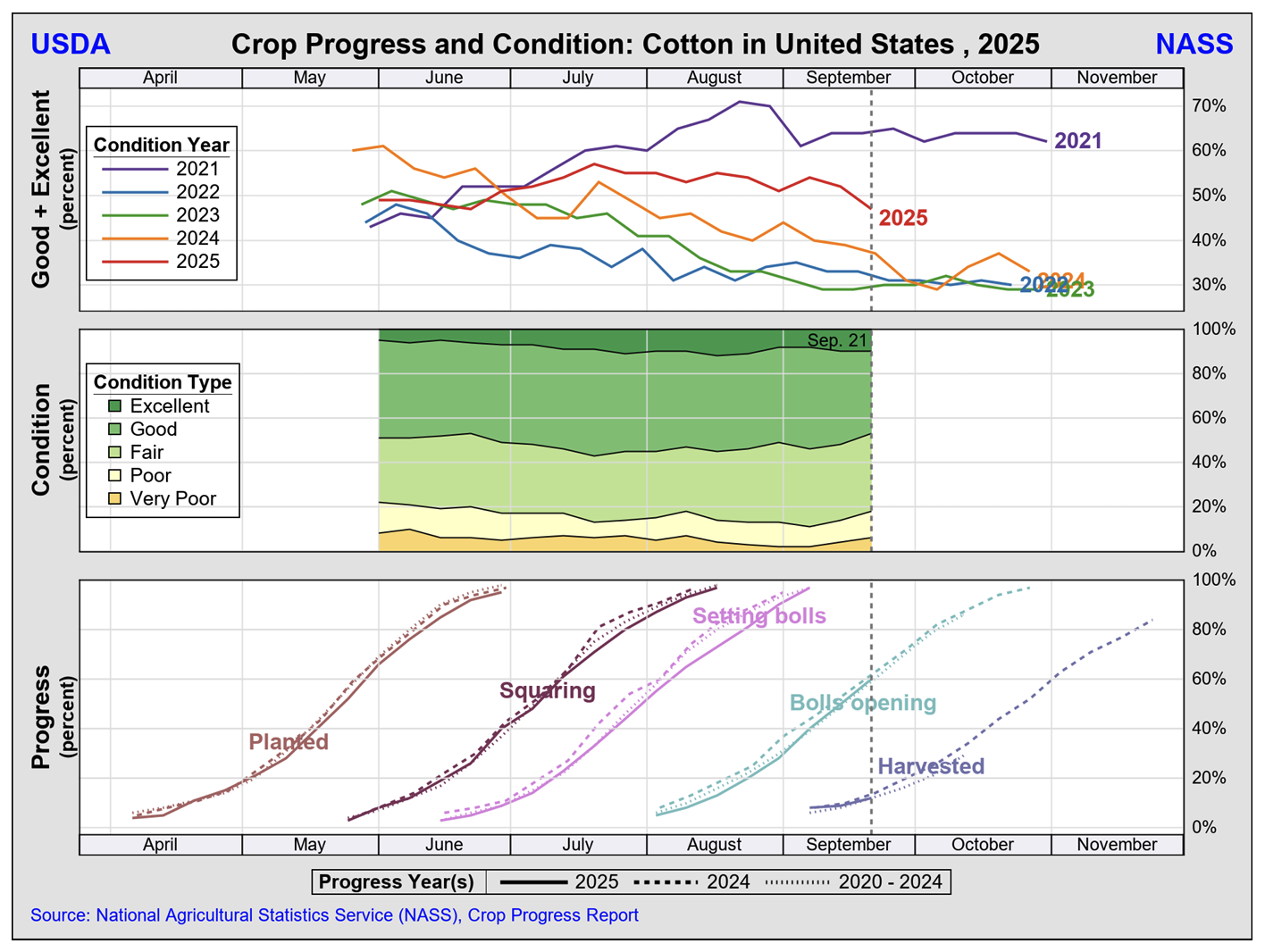

Weather and Crop Watch

Southwest crop conditions remain mostly favorable. Oklahoma was the only state with a higher percentage rated good to excellent, increasing to 69%. Texas decreased to 41%, and Kansas decreased to 58%. Boll opening has reached 53% in Texas, 57% in Oklahoma, and 22% in Kansas. Harvest is winding down in South Texas, with more than 85% complete, bringing the statewide harvest to 23%.

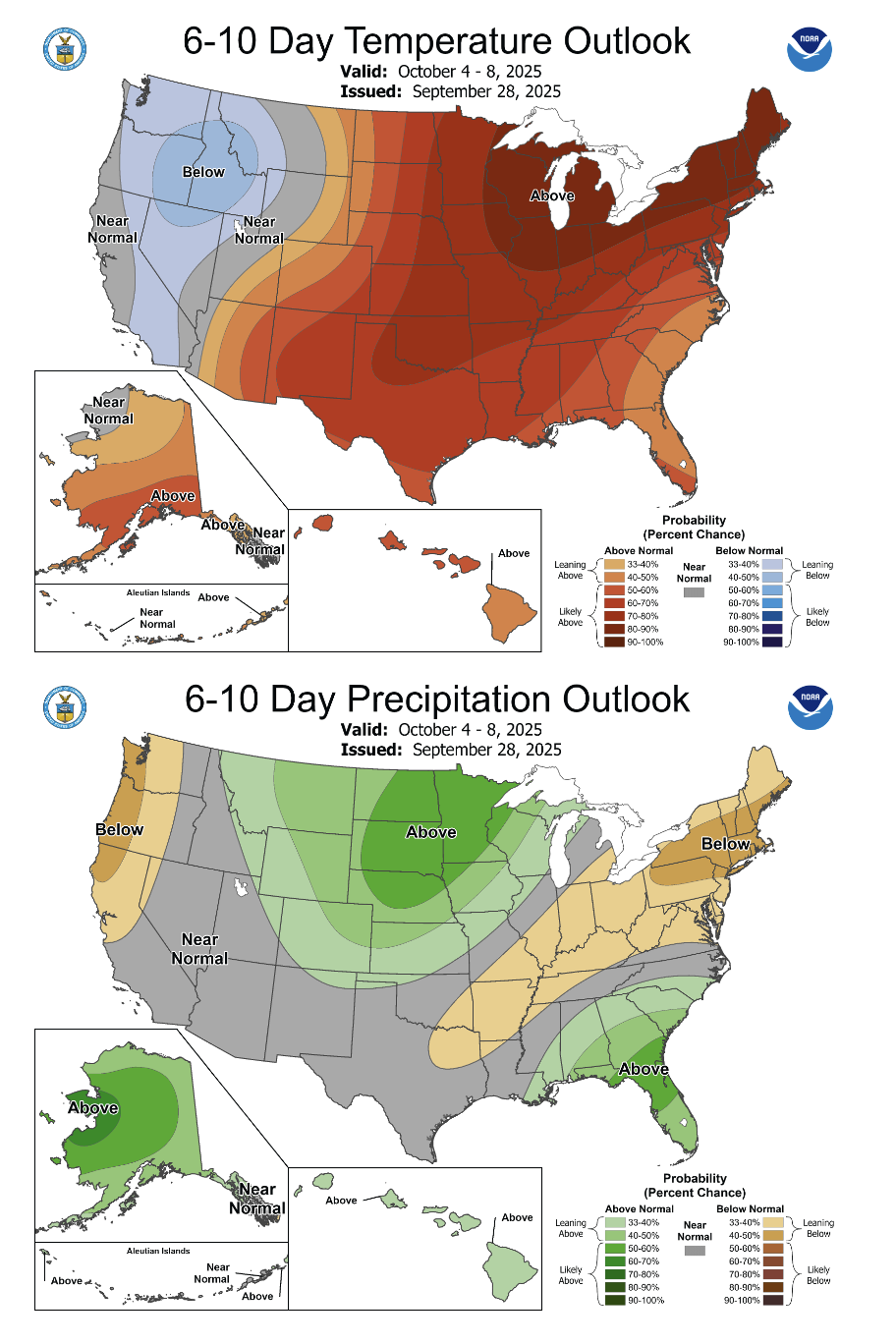

West Texas stayed mostly dry over the weekend, though light showers fell in the Rolling Plains and South Texas, where harvest progress slowed. Quality in South Texas remains strong, but scattered rain has the potential to cause some discoloration in open cotton. Above-average temperatures and average precipitation are expected, favoring boll maturation across West Texas, Oklahoma, and Kansas. Overall, conditions look supportive for continued crop development and for South Texas harvest to wrap up with only brief weather interruptions.

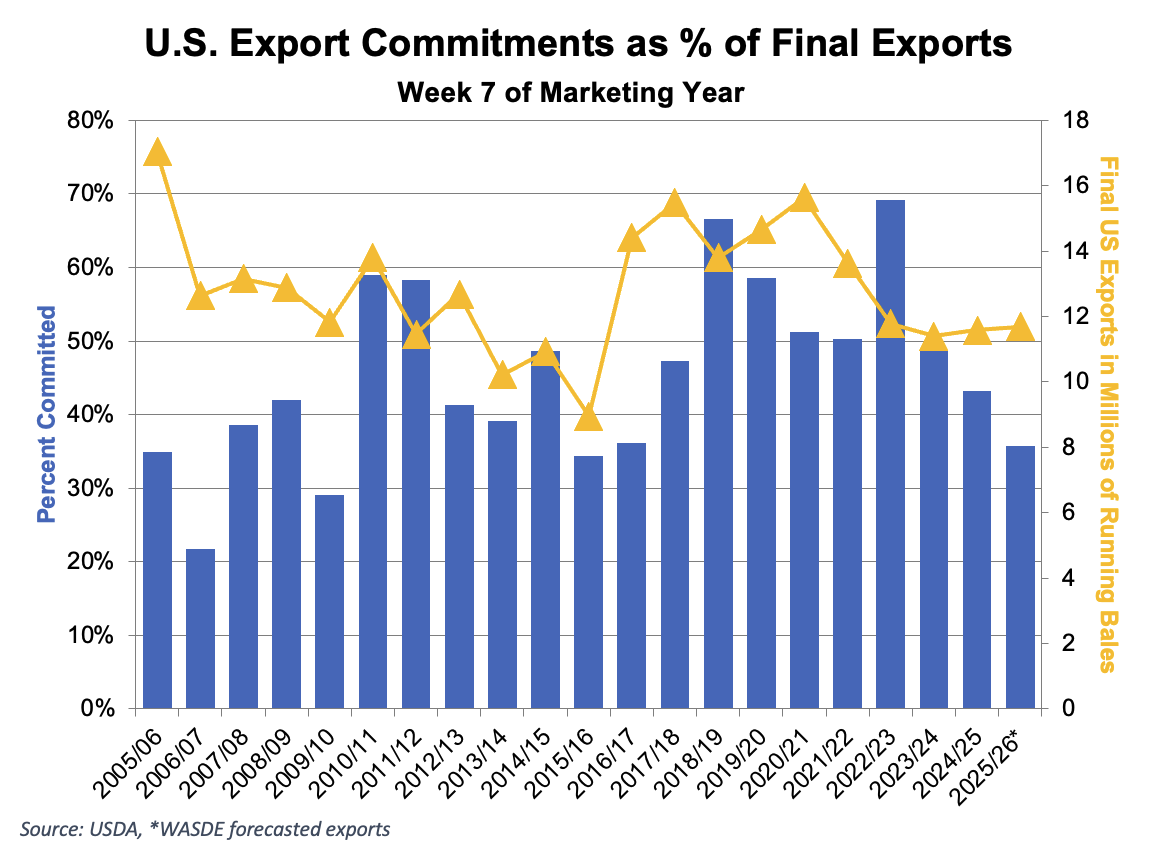

Export Trends

Export sales slowed this week, with net Upland bookings of just 86,100 bales. The pullback likely reflects the recent price run-up and the fact that buyers are able to source cotton from competing origins. India led with 27,300 bales, followed by Turkey, Bangladesh, and Vietnam. Cancellations were minimal, and no new-crop sales were reported. Overall, commitments remain light, consistent with weaker demand and seasonal lulls.

Shipments were slightly higher, with 137,200 bales getting exported for the week. This slower pace reflects ongoing competition from other growths and limited U.S. availability.

For Pima, sales were solid for this point in the season at 8,500 bales, led by Colombia, while shipments of 5,200 bales kept both sales and exports running ahead of the pace needed to meet USDA’s target.

The Seam

As of Thursday afternoon, grower offers totaled 24,639 bales. There were 2,562 bales that traded on the G2B platform that received an average price of 63.14 cents per pound. The average loan for these bales was 55.80, bringing the average premium received to 7.34 cents per pound.

Latest News

GUJCOT WEEKLY REPORT 31-JAN-2026

Market Movement from 26th Jan 2026 to 31st Jan 2026.

• NY March futures traded in a narrow rang