We’re 34 days into the shutdown, with leaders still holding firm. Some movement is happening behind the scenes as senators work on FY2026 spending, and the restart of SNAP payments offers a bit of relief. Markets are starting the week cautiously after Powell cooled expectations for a December rate cut, keeping the dollar firm and risk appetite limited. Attention now shifts to Wednesday’s ADP jobs report, a read on private-sector hiring, and to major commodity earnings for clues on demand and margins. Ag markets are steady on improved trade tone and favorable weather, though fund flows and index shifts could bring short-term volatility. With harvest in full swing and the November WASDE delayed to the 14th, cotton and other commodities will likely trade with the broader macro mood and currency movement.

While updated cotton-specific details aren’t yet available, the CCC loan program is expected to reopen to producers soon. There’s still no formal confirmation for cotton, but signs point to progress behind the scenes. A long-term solution is still needed to prevent future disruptions, yet this reopening is a crucial step—restoring a key safety net growers have gone without for weeks.

Market Recap

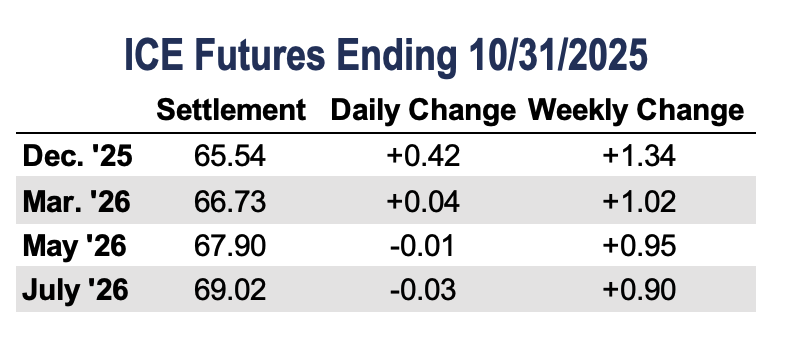

Cotton futures rose in four of five sessions last week, supported by steady demand, improved technicals, and light trade optimism. December futures gained 134 points on the week, settling at 65.54 cents per pound.

Most of the activity centered on heavy December spread trading during the Rogers Index Roll, which wraps up today, with the Goldman Roll set to begin Wednesday. December options expire Friday and could add another round of volatility as traders square positions. Overall, prices are holding near recent highs, and while short-term technical momentum improved last week, longer-term trends remain flat. The market enters mid-November on relatively firm footing despite ongoing macro and policy uncertainty.

Daily trading volume was strong last week amid positive trade developments, and open interest rose 2,451 contracts to 297,502. Certified stocks declined by 3,803 bales to 13,749.

Economic and Policy Outlook

The Trump–Xi summit last week marked a major breakthrough, with both sides agreeing to suspend tariffs and reopen agricultural and industrial trade flows. China’s removal of duties on U.S. cotton, soybeans, and other farm goods is welcome news, while the U.S. has agreed to ease select tariffs and pause certain trade enforcement measures. Cotton futures—after climbing for most of last week—showed only a muted reaction to the announcement, a classic “buy the rumor, sell the fact” move. Even so, the deal steadies sentiment and supports a firmer outlook for U.S. ag trade heading into year-end.

The Fed cut rates by a quarter point to 3.75–4% but struck a cautious tone, with Powell warning another move in December is “far from certain.” His remarks cooled rate-cut expectations, lifted the dollar, and pressured risk assets, signaling a short-term headwind for commodities. For cotton, the stronger dollar and hawkish tone could continue to temper export demand near term, but the broader shift toward easier policy and stable inflation still supports a constructive outlook once markets adjust.

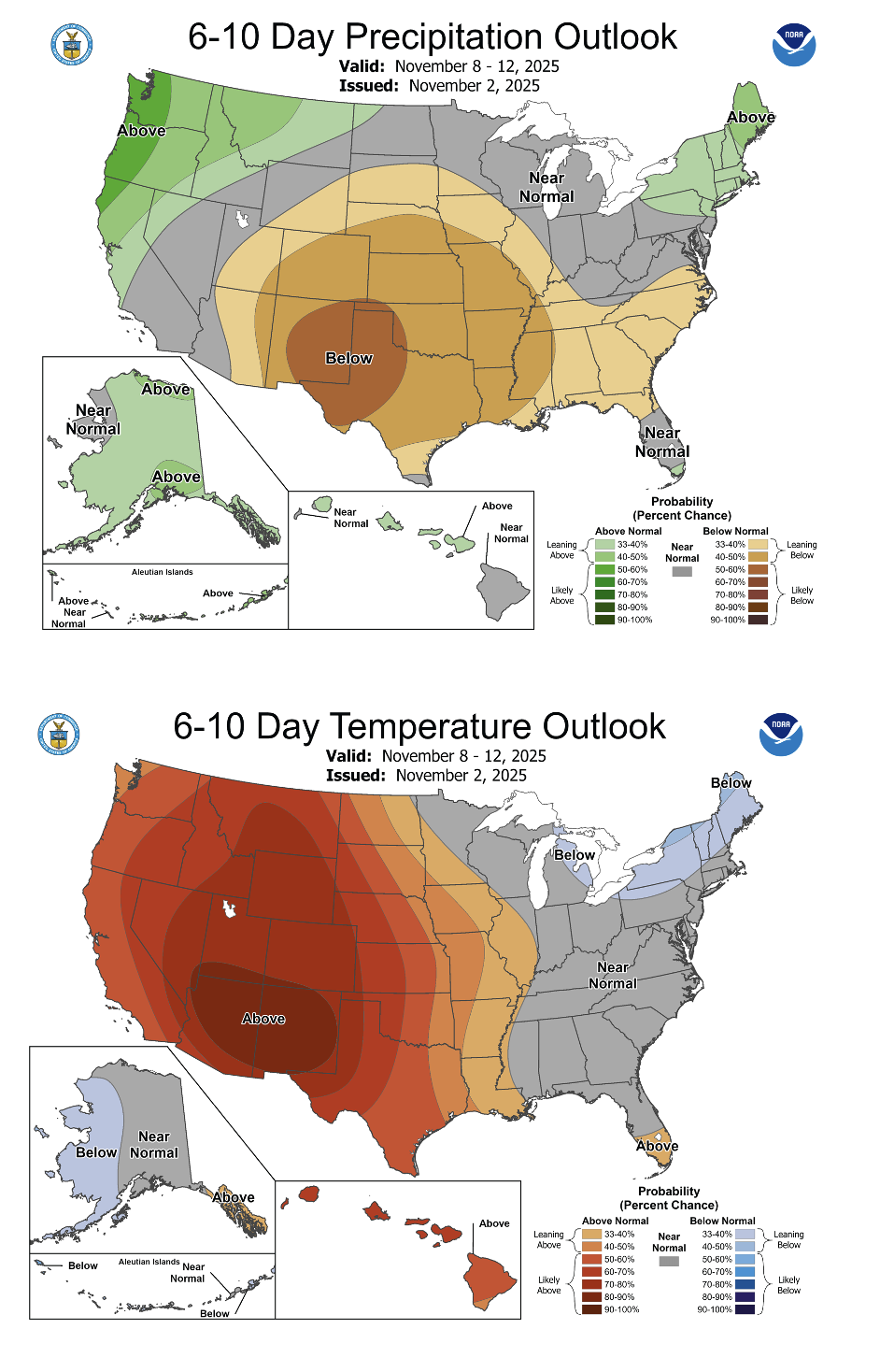

Weather and Crop Watch

Dry, mostly favorable conditions across western Texas and southwestern Oklahoma supported fieldwork over the weekend, with only light rain in southern areas. Last week’s freeze brought mixed effects—helping firm up open cotton and advance harvest in some areas while halting boll development elsewhere, which could affect the quality of later harvested fields. The next two weeks look largely dry, allowing progress to continue with only a few scattered showers. It looks to be a pleasant stretch overall, with a brief cooldown late this week followed by warmer conditions early next week. Early classing shows strong quality in most areas, particularly around Abilene and Lubbock, while Lamesa cotton is grading slightly shorter, resulting in slightly softer loan values.

The Seam

As of Friday afternoon, grower offers totaled 29,660 bales. The past week 13,767 bales traded on the G2B platform received an average price of 60.94 cents per pound. The average loan was 53.92, bringing the average premium received to 7.02 cents per pound.

No official Adjusted World Price (AWP) data release from USDA due to the government shutdown.

Latest News

U.S. EXPORT SALES

For Week Ending 05-Feb-2026

2025-2026

Net Upland Sales 2,31,000

Upland Shipments 1,88,600

Ne