Much to everyone’s relief, there finally appears to be an end in sight to the government shutdown, now in its 41st day and the longest in U.S. history. The Senate voted 60 to 40 late Sunday to advance a stopgap funding bill to reopen the government through January 30, paired with a three-bill minibus that provides full funding for Fiscal Year 2026 for Military Construction and Veterans Affairs, Agriculture, and the Legislative Branch. This means USDA should be able to keep the loan program running even if another shutdown occurs in January, which is a significant improvement after the issues we’ve seen this time. The House still needs to approve the measure before it can reach the President’s desk. While progress is being made, the final steps could still be bumpy. Markets rallied on the news, opening higher on the day, and that strength carried over into the commodity sector as well.

This will also be a busy week for commodities. The CCC loan program has officially reopened to producers after some earlier delays, and USDA will release its first supply and demand update since the shutdown began. The WASDE report is scheduled for November 14 at 11:00 a.m. CST — slightly delayed but highly anticipated. For cotton, analysts largely expect the U.S. crop estimate to rise from the current 13.2 million bales.

Market Recap

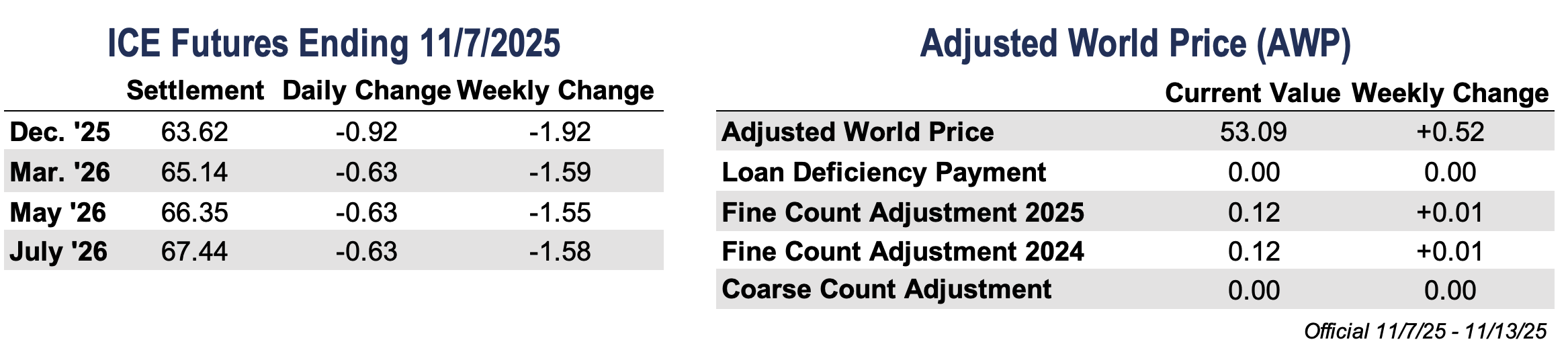

Despite this week’s positive developments, cotton prices struggled last week. December futures fell in every session, ending the week 192 points lower at 63.62 cents per pound.

Heavy index rolling, as the biggest of funds began shifting their positions forward, along with option expiration and broader “risk-off” sentiment, weighed on the market throughout the week. Early optimism over reports that China would lift retaliatory tariffs quickly faded, and selling intensified midweek amid one of the highest volume sessions on record. Open interest reached multi-year highs, reflecting strong participation despite weaker prices. Traders now look ahead to Friday’s WASDE report for fresh direction.

Daily trading volume was strong last week, and open interest rose 1,628 contracts to 295,874. Certificated stocks were unchanged at 13,749 bales.

Economic and Policy Outlook

The record-long U.S. government shutdown has left investors flying blind, with key economic data – including jobs and inflation reports – delayed for weeks. Lawmakers are beginning to move toward reopening the government, but it could still take time for a final agreement to become law. Once operations resume, markets will face a wave of backlogged data, starting with the long-delayed jobs report, though inflation figures may take even longer to compile. The lack of timely information complicates the Federal Reserve’s decisions on interest rates ahead of its next meeting. Despite the uncertainty, stocks and bonds have remained near record highs as investors bet the Fed will stay inclined to cut rates.

The Supreme Court appears poised to limit President Trump’s tariff powers, marking a potential turning point as public opinion and economic pressures shift. Even so, Trump has doubled down with a proposal for a $2,000 “tariff dividend” for Americans, an expensive idea that surprised his own Treasury secretary. Support for tariffs has eroded as voters report higher costs and as the slowing economy weighs on businesses. Together, these trends suggest that the United States may have reached a peak in tariffs, both politically and economically.

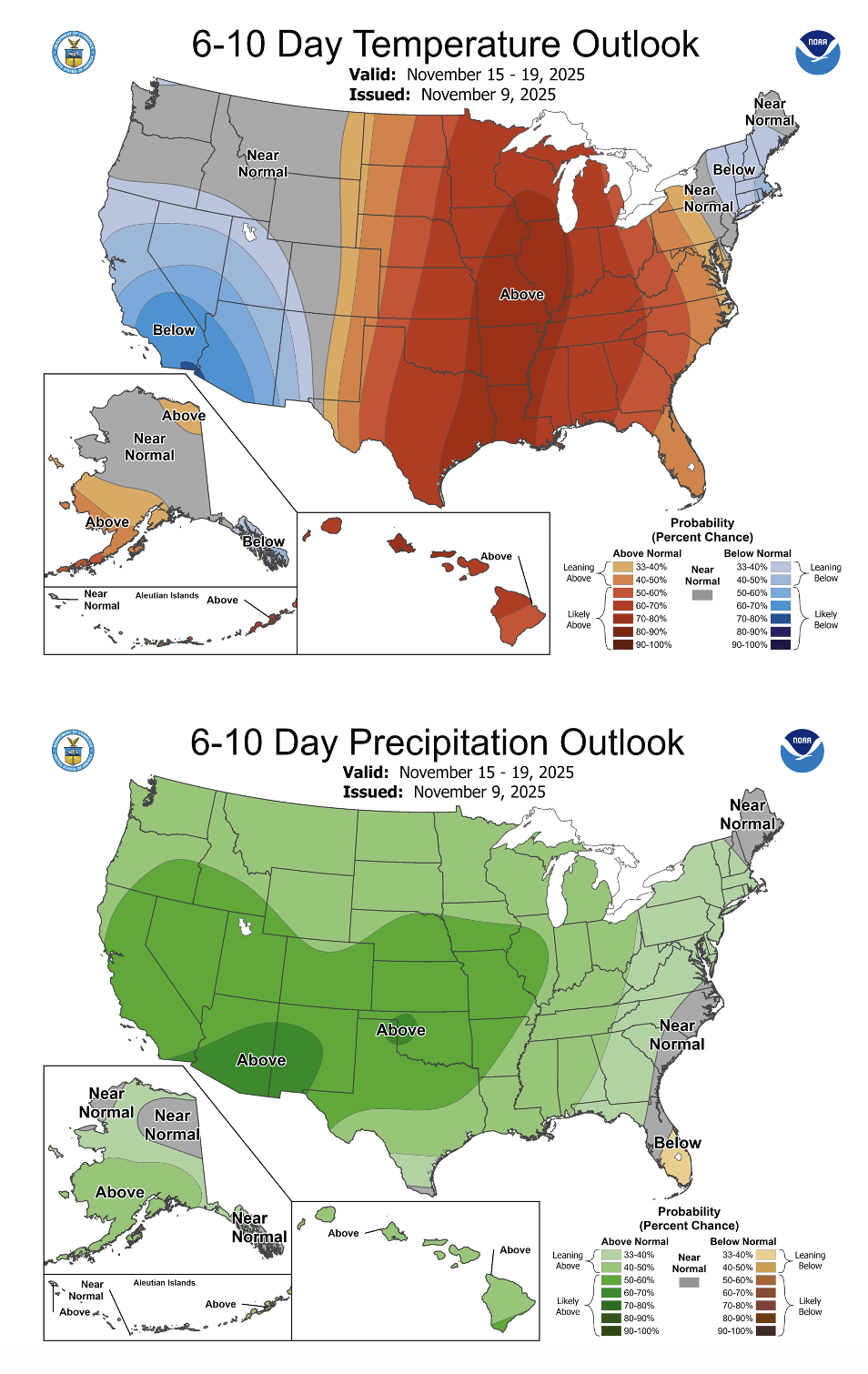

Weather and Crop Watch

Mild, mostly dry conditions are expected across the Southwest this week, offering a favorable window for harvest progress. Temperatures will run well above normal early in the week, reaching the upper 70s to low 80s under mostly sunny skies. Winds may be gusty at times before easing midweek, followed by a weak front this weekend that could bring a short-lived cooldown and a slight chance of light showers. Overall, field conditions should remain supportive for steady harvest activity. Harvest weather remains broadly favorable across the Southwest and much of the Cotton Belt. Cooler temperatures are helping wrap up the growing season, while limited rainfall and mostly sunny skies will keep fieldwork and ginning moving efficiently.

Quality across the region continues to grade well at the local classing offices. Lubbock cotton continues to improve, Abilene is holding steady, and while Lamesa’s quality has been somewhat lower, it remains consistent with past seasons.

The Seam

As of Friday afternoon, grower offers totaled 36,584 bales. The past week 9,983 bales traded on the G2B platform received an average price of 62.92 cents per pound. The average loan was 54.98, bringing the average premium received to 7.94 cents per pound.

Latest News

U.S. EXPORT SALES

For Week Ending 05-Feb-2026

2025-2026

Net Upland Sales 2,31,000

Upland Shipments 1,88,600

Ne