Markets start the week on a cautiously bullish footing as traders look ahead to Wednesday’s Fed decision, where a rate cut is widely expected. Tuesday’s WASDE could draw more attention than usual, arriving alongside a wave of delayed USDA and CFTC reports. China remains a swing factor after mixed signals on purchase commitments, even as officials reaffirm broader cooperation and continue working through trade agreements. SDRP Stage 2 payments are starting to roll out, though growers remain wary after earlier delays. Many are also watching for the approximate $12 billion farm-aid package that’s expected to be announced today, but the timing is not guaranteed even with a tentative 1:00 p.m. CST slot. With major macro events and catch-up data all landing at once, markets are set up for a volatile stretch.

Market Recap

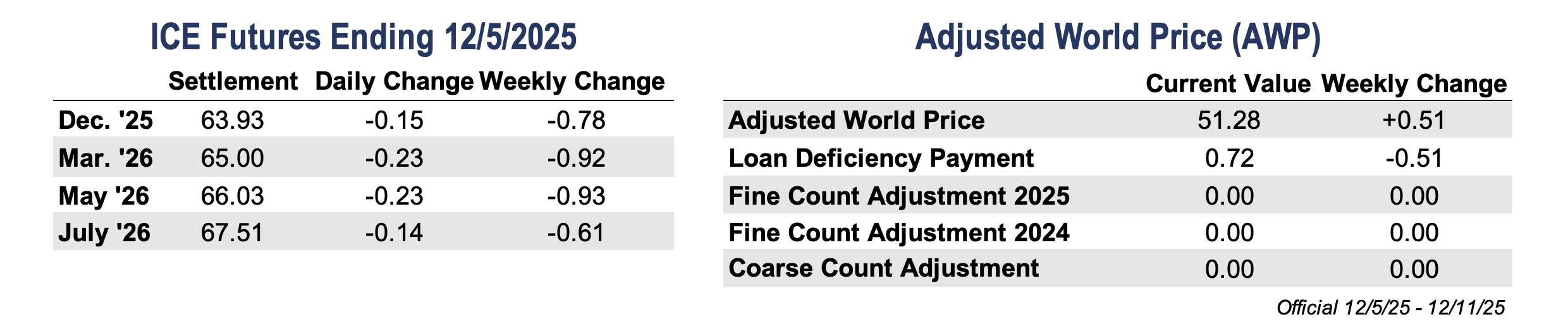

Cotton futures started December on a softer note, settling lower each day last week and keeping the overall trend relatively flat. March futures gave up 78 points over the week and closed at 63.93 cents per pound.

It was a quiet stretch for cotton-specific news, and much of the focus remained on government shutdown–delayed reports that are slowly catching up. The Cotton On-Call report is now current, but Export Sales and the Commitments of Traders report are still being released on a delayed schedule and have not fully caught up. The latest On-Call data showed the smallest sales–purchase imbalance of the season, and the most recent (though still outdated) CFTC report indicated specs were net buyers for the week ending October 28, ahead of a late-month rally; even so, speculative traders remain heavily net short overall. March futures also tracked broader markets, which opened the week under pressure after U.S. manufacturing posted its ninth consecutive monthly decline. The tone stayed muted throughout the week, with technicals still pointing lower.

Daily volume was on the quieter side, with open interest rising 8,043 contracts to 286,741. Additionally, 4,759 bales were decertified, bringing certificated stocks to 15,585 bales.

Supply and Demand Overview

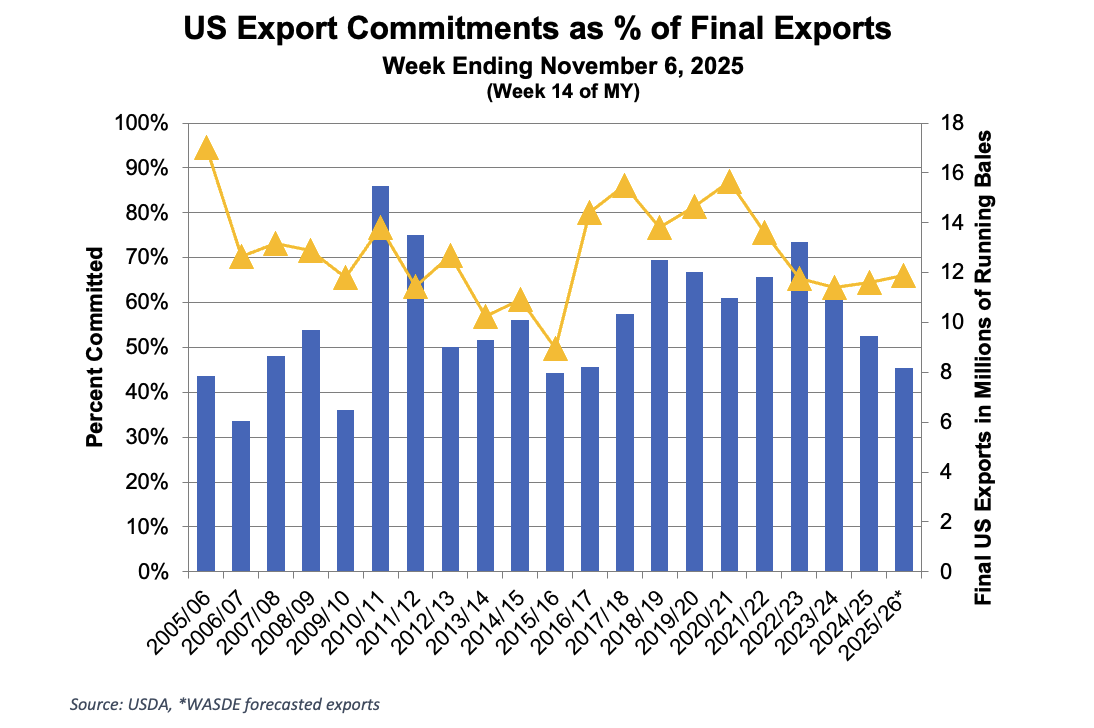

USDA released two more delayed Export Sales reports over the last week, giving us a clearer picture of late October and early November demand. Surprisingly, given the demand environment, the reports have been mixed, but overall better than expected.

For the week ending October 30, net Upland sales totaled 81,500 bales, with shipments at 146,600 bales. Pima bookings were 8,200 bales, with 2,700 bales shipped. While the market does not necessarily react to data this old, it still provides context for where demand stood and highlights that shipments remained behind USDA’s 12.2-million-bale target.

The Export Sales report for the week ending November 6 showed a marketing-year high in Upland sales. Net bookings reached 292,100 bales, led by Vietnam, Mexico, and Turkey, while shipments totaled 135,900 bales. Pima sales reached 6,000 bales, with exports at 3,800 bales. This was one of the stronger reports of the 2025 marketing year. Another Export Sales report will be released Thursday as USDA continues working through the delayed schedule.

Economic and Policy Outlook

Last week brought a busier run of data and headlines than we’ve seen recently, and the labor market once again delivered mixed signals. ADP, which tracks private-sector payrolls, showed employment falling by 32,000 jobs in November, its softest reading since 2023, with payrolls now down in four of the past six months. Analysts had expected a small increase, making the downside surprise more notable. At the same time, jobless claims fell to their lowest level in more than three years, though this series can swing sharply from week to week, so the market tends not to put too much weight on a single report.

The U.S. dollar weakened on the softer labor data, offering some support to commodities. The Chinese yuan was firmer, and the Brazilian real had also been strengthening until late last week, when political turmoil and government announcements triggered a sharp drop in the currency, adding fresh pressure to commodity markets. Taken together, the week’s economic signals left traders all but fully pricing in a Fed rate cut at the meeting taking place Tuesday and Wednesday, with the decision set for release at 1 p.m. CST on Wednesday.

September’s Personal Consumption Expenditures (PCE) report was also released – now two months old – and largely aligned with expectations, rising 0.3% on the month and 2.8% year over year. While upcoming jobs and CPI data will matter far more for the Fed’s path, the PCE rate still offered a snapshot of where inflation stood heading into the fall.

Weather and Crop Watch

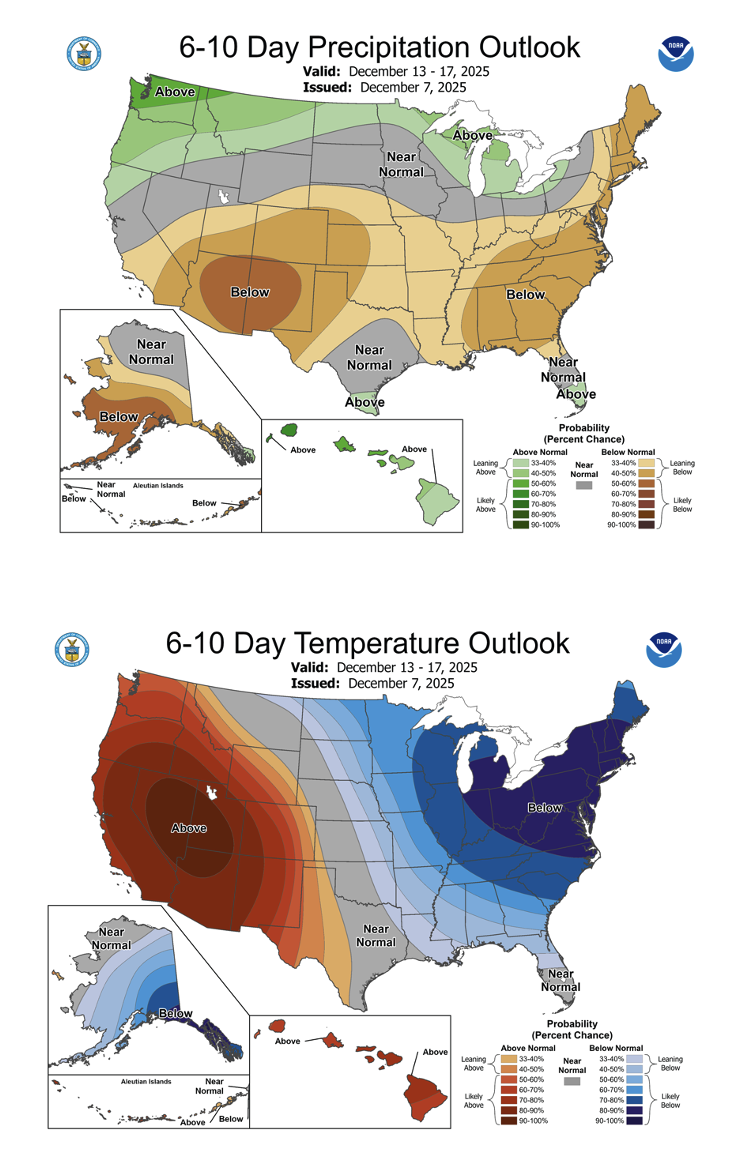

Harvest is now winding down across the Southwest as most growers push through the last of their acres. A burst of cold weather earlier in the week helped finish off any lingering fields, and the forecast should cooperate as we head into the next several days. West Texas and nearby areas are expected to stay mostly dry with seasonally mild temperatures, and while a few pockets could see light showers, nothing suggests any notable slowdowns. Overall, conditions look steady and workable, giving producers a clean window to bring the remainder of the crop in.

The 2025 season in South Texas is essentially finished, with the Corpus Christi office wrapping up for the year. West Texas classing offices saw a slight decrease in loan values over the past week, but overall quality remains strong. Lower-quality cotton has been limited and mainly tied to a bit more bark and slightly lower micronaire, while other measures remain steady and well above normal for the region. Early Southwest results continue to show strong, consistent quality as more cotton moves through the classing offices.

The Seam

As of Friday afternoon, grower offers totaled 112,702 bales. The past week 36,451 bales traded on the G2B platform received an average price of 60.44 cents per pound. The average loan redemption rate (LRR) was 53.25, bringing the average premium over the LRR to 7.19 cents per pound.

*Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).

Latest News

GUJCOT WEEKLY REPORT 31-JAN-2026

Market Movement from 26th Jan 2026 to 31st Jan 2026.

• NY March futures traded in a narrow rang