Holiday trading carried through year-end as markets looked ahead to 2026. The year started off relatively quiet, but geopolitical tensions between the U.S. and Venezuela could inject some volatility into energy markets. Beyond that, attention is shifting to a busier data calendar that may help set the tone early in the year. Updated trade deficit and consumer credit data are due Thursday, January 8, followed by jobs data and the unemployment rate on Friday, January 9. Annual index fund rebalancing also begins Thursday, and while some buying in cotton is expected, it is likely to be more muted than in recent years.

In cotton, focus is shifting to the upcoming supply and demand analysis from USDA on Monday, January 12 at 11:00 a.m. CST, which may bring additional clarity after lingering questions around December’s state-by-state adjustments. While most analysts agreed with the overall crop estimate of 14.27 million bales, the regional details will matter as the market looks for confirmation, or revision, heading into 2026.

Market Recap

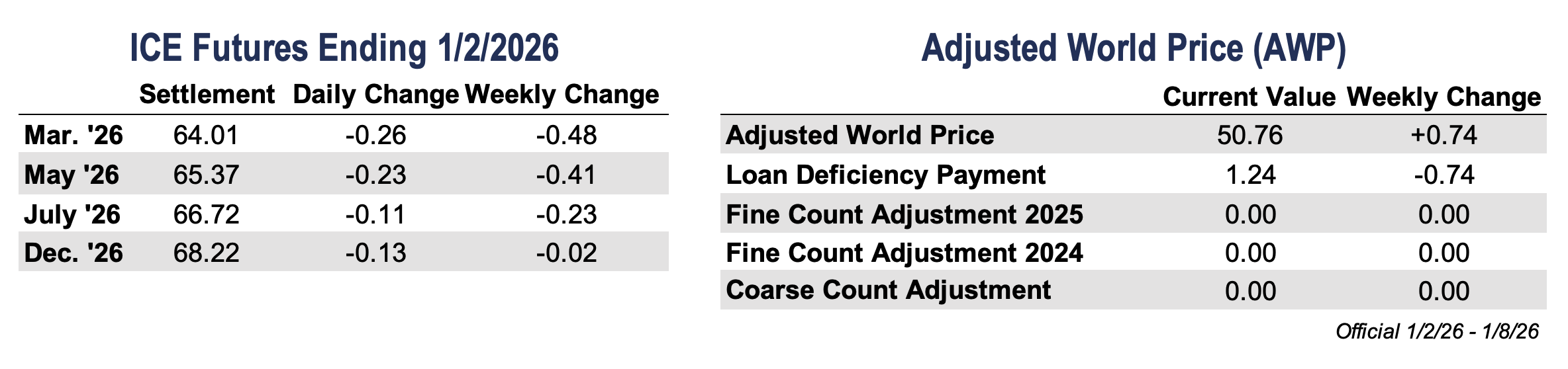

March futures finished lower in each trading session last week, with only four sessions due to the New Year’s holiday this past Thursday. Despite the consistent pressure, the overall weekly decline was relatively modest. On Friday, March futures settled at 64.01 cents per pound, down 48 points on the week.

Holiday trading schedules over the past couple of weeks have kept markets relatively quiet, though a few developments stood out. Notably, the Indian government announced that its 11% cotton import duty was reinstated, beginning January 1, 2026. The recent move lower may reflect a combination of grower selling and hedging tied to loan redemptions, along with the market running into technical resistance before turning back down. Even so, updated Commitments of Traders data, now fully caught up, show that speculators have meaningfully reduced their short positions in recent weeks, a shift worth monitoring going forward.

Oddly enough, trading volume picked up on the first trading day of 2026, reaching the highest daily volume traded level in the two weeks of holidays. Total open interest saw a marginal increase of 4,426 contracts to 304,963 Additionally, 90 bales were decertified over the past week, bringing certificated stocks down to 11,510 bales.

Economic and Policy Outlook

2025 turned into a year of adjustment across global markets, with shifting U.S. trade policy, higher tariffs, and policy uncertainty driving volatility in trade flows, currencies, and broader risk sentiment. Global trade held up better than expected, but U.S. imports slowed and supply chains began to work around a more protectionist backdrop. Financial markets reflected that tension, with globally diversified assets and hedge funds benefiting from volatility, while the U.S. dollar posted its worst annual performance since 2017 amid growing expectations for Fed rate cuts.

Heading into 2026, the focus is shifting from the shock of tariffs to their longer-term consequences, with markets also awaiting a Supreme Court decision that could influence how those tariffs are enforced. Policy swings may be less abrupt, but slower U.S. import growth, ongoing trade negotiations, and lingering legal uncertainty suggest trade friction isn’t going away. With Fed leadership changes on the horizon and rate-cut expectations still in play, markets remain sensitive to policy signals as the new year unfolds. To be clear, the more of these matters that get settled, the better the trading environment for cotton.

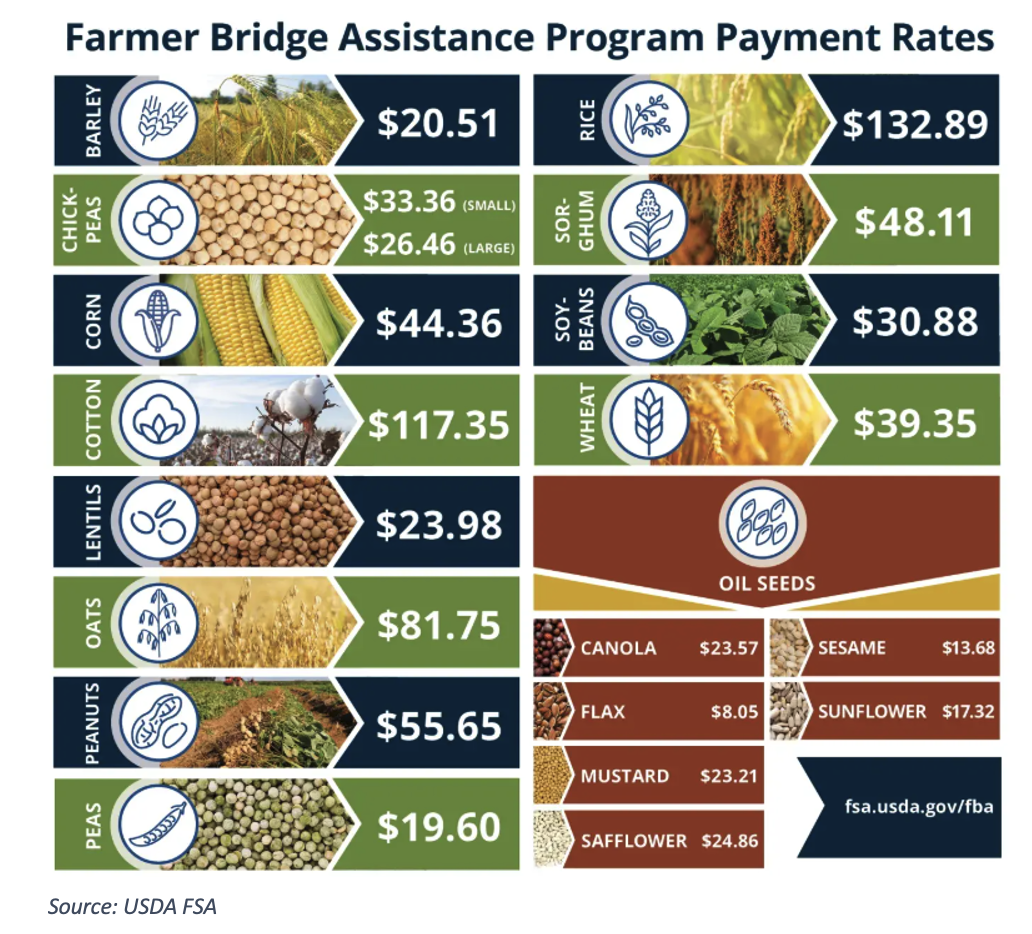

USDA’s Farm Service Agency has announced a one-time Farmer Bridge Assistance (FBA) Program, providing $11 billion in near-term support to help producers bridge the gap until longer-term farm policy relief becomes available. Payment rates were released on December 31, with cotton set at $117.35 per eligible acre. Eligible producers must be actively engaged in farming and have reported 2025 planted acres by the December 19 deadline. Payments are expected to begin by February 28, 2026, while USDA continues developing details for an additional $1 billion reserved for commodities not currently covered. In a pivot from recent ad-hoc programs, USDA lowered the payment limit from $250,000 to $155,000 per person or legal entity, including corporations, limited liability companies, S corporations, and trusts.

Supply and Demand Overview

The two weeks of export sales reported last week were respectable, but still underwhelming from a sales perspective. For the week ending December 18, net Upland sales totaled 304,700 bales, while shipments lagged at 182,700 bales. Vietnam, Pakistan, and Bangladesh were the primary buyers, with China reappearing on the report but in smaller volumes. Pima sales reached 9,100 bales, with 7,200 bales shipped.

For the week ending December 25, net Upland sales slowed to 134,000 bales, though shipments increased to 140,700 bales. Vietnam, Pakistan, and Turkey led buying interest. Pima sales totaled 3,100 bales, while exports rose to 10,900 bales. The next Export Sales Report is scheduled for Thursday, January 8, at 7:30 a.m. CST, with USDA expected to be fully caught up on data delays tied to the government shutdown.

The Seam

As of Friday afternoon, grower offers totaled 114,686 bales. The past week 56,266 bales traded on the G2B platform received an average price of 61.16 cents per pound. The average loan redemption rate (LRR) was 52.05, bringing the average premium over the LRR to 9.11 cents per pound.

Latest News

Cleveland on Cotton 05-Jan-2026

A Chinese New Year that Lifts Cotton Prices?

The New Year begins a bit brighter than Auld Lang Sy