PCCA Cotton Market Weekly 02-Feb-2026

Posted : May 23, 2026

February 2, 2026

The Week Ahead

Risk appetite is cautious to start February, with policy uncertainty and a busy week of data keeping markets on watch.

- Markets start the week on a cautious note, with a sharp selloff in precious metals weighing on broader risk sentiment. Attention now shifts to a heavy slate of earnings and key economic releases, the most watched being unemployment data, that could set the tone for the next leg of trading.

- Washington faces another messy week as House Republicans struggle to advance a Senate-backed funding deal amid internal divisions over DHS and ICE policy. With the shutdown already underway and little room for error, the next few days will determine whether leadership can unify votes or the standoff drags on further.

- On a more lighthearted note, Punxsutawney Phil saw his shadow this morning – meaning winter isn’t quite done yet, with six more weeks of cold weather likely ahead.

February has started off busy for the cotton market. The crop insurance price discovery period for much of the Southwest began February 1, and as a reminder, the cotton insurance price for the southernmost portion of Texas was set at 68 cents per pound for the 2026 crop year. This week also brings March options expiration on Friday, with an updated USDA supply and demand report due next Tuesday, February 10. Looking ahead, the coming weeks will deliver a series of acreage updates and early projections that should provide the first clearer signals of what 2026 cotton plantings may look like.

Market Recap

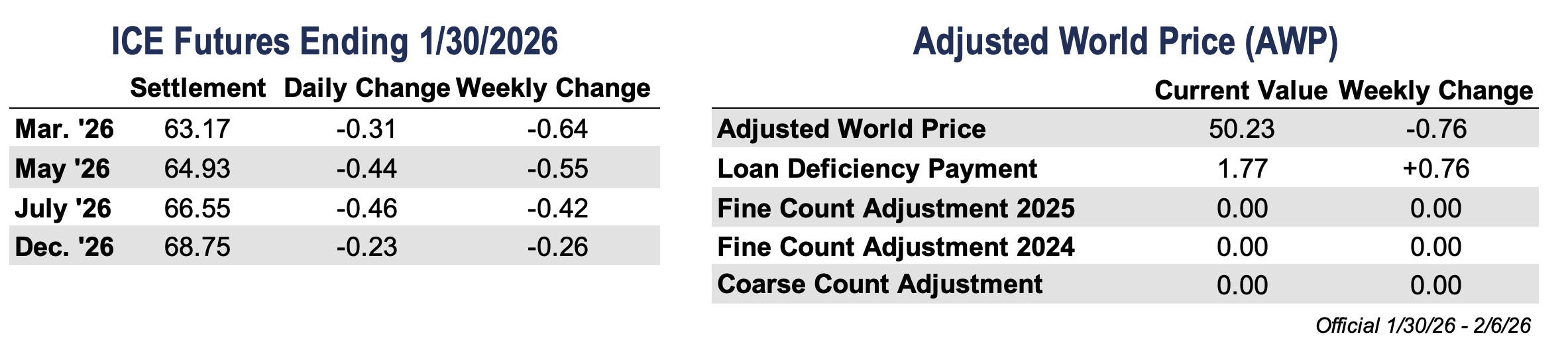

- Although it may have felt like March futures took a bigger hit, the contract finished last Friday down 64 points, settling at 63.17 cents per pound. As traders begin rolling positions forward to May, coverage will shift to the new front month. May futures ended the week 55 points lower, closing at 64.93 cents per pound.

- March futures posted another contract low last week, though prices saw a brief bounce the following day as the U.S. dollar slipped to its weakest level since early 2022. The Export Sales Report offered little support, and the Cotton On-Call report continues to highlight a significant imbalance in unfixed commitments. One notable development was speculators making one of their largest weekly additions to net short positions – a key driver behind the latest leg lower in cotton prices, even as they have remained net short for more than 90 weeks.

- Weakness was seen across the broader softs complex as well, with cocoa and coffee hit especially hard on Friday, underscoring the widespread volatility. Overall, technical momentum remains weak as major index funds continue to roll, and with added uncertainty from geopolitical and U.S. economic developments, the week ahead could be an active one.

- Daily volume was strong last week, and open interest continued to build. Total open interest reached record levels, increasing by 24,072 contracts to 372,796, while certificated stocks increased 15,244 bales to 25,666 bales.

Economic and Policy Outlook

- Markets had plenty to digest this past week after President Trump tapped Kevin Warsh to lead the Federal Reserve, a pick traders took as more hawkish. Stocks slid while Treasury yields pushed higher as expectations around interest rates shifted. The dollar also caught a bit of a bounce after selling off earlier in the week, though it’s still sitting at fairly low levels. Gold and silver were hit hard as investors adjusted to the changing policy outlook. Oil prices eased for now, but Iran-related risks remain an overhang. All in all, it was another reminder of how quickly sentiment can shift when policy and geopolitics collide.

- Lawmakers moved late last week to avoid a prolonged government shutdown, with the Senate passing a short-term funding package. Still, several agencies were expected to face at least a brief lapse in funding as the House delayed action until today, February 2. While disruptions are likely to be limited if the issue is resolved quickly, the episode highlights ongoing political uncertainty tied to broader immigration negotiations. Markets and agencies will be watching closely this week for a swift resolution and a clearer path forward on federal funding.

- The Fed left rates unchanged this past week, holding the policy range at 3.50%–3.75% as officials signaled growing confidence in the economy’s resilience. Powell acknowledged inflation remains somewhat elevated, but said risks to both employment and prices have eased, reinforcing expectations for an extended pause. Two dissenting votes in favor of a cut added a dovish undertone, though the broader message was patience. Markets took the decision in stride, with investors now looking toward mid-year for the next potential rate move.

Supply and Demand Overview

- The Export Sales Report for the week ending January 22 showed marketing-year high shipments for Upland cotton and marketing-year high sales for Pima. Net Upland sales totaled 203,700 bales, while Pima sales came in at 24,800 bales. Shipments were also strong, with 257,000 bales of Upland exported during the week, along with 4,500 bales of Pima.

- Despite the headline numbers, the market was not overly impressed, as export business remains inconsistent and highly dependent on what can be competitively offered. Even with marketing-year high shipments, exports will need to remain at or above this pace to meet USDA’s 12.2 million bale forecast. Sales must average roughly 195,000 bales per week, with shipments closer to 300,000 bales per week to stay on track.

- One positive development over the weekend was news that garments produced in Bangladesh using U.S. cotton are expected to receive duty-free access to the U.S. market, while Bangladesh’s reciprocal tariff rate could fall from 20% to 15%. The agreement is expected to be signed in Washington on February 9. Bangladesh has been appearing more frequently in recent export reports and could represent a market with growing potential for U.S. cotton demand.

The Seam®

- As of Friday afternoon, grower offers totaled 125,548 bales. The past week, 31,158 bales traded on the G2B platform received an average price of 57.77 cents per pound. The average loan redemption rate (LRR) was 49.88, bringing the average premium over the LRR to 7.89 cents per pound.

Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).

Sustainability Enrollment Windows

- Enrollment for the U.S. Cotton Trust Protocol will be open from January 5 to April 30, 2026. Growers who are currently enrolled will need to renew their membership to continue their involvement in the program. If your gin would like to host an Enrollment Field Day during this time, please reach out to PCCA at (806)762-8011.

- New Grower Enrollment for the Better Cotton Initiative will be open from March 3 to May 30. Growers interested in joining this global sustainability program should contact PCCA (806) 763-8011.