February 16, 2026

The Week Ahead

Markets enter a holiday-shortened but event-heavy week, with macro data and policy headlines likely to set the tone. U.S. markets are closed today, February 16. When trading resumes tomorrow, it should be back to business as usual.

- Fed minutes, GDP, and PCE inflation are on deck later this week. The macro mood turned more cautious on Friday as equities softened, but a weaker dollar continues to offer support to commodity markets. Any move in the dollar or shift in rate expectations could influence near-term direction for cotton.

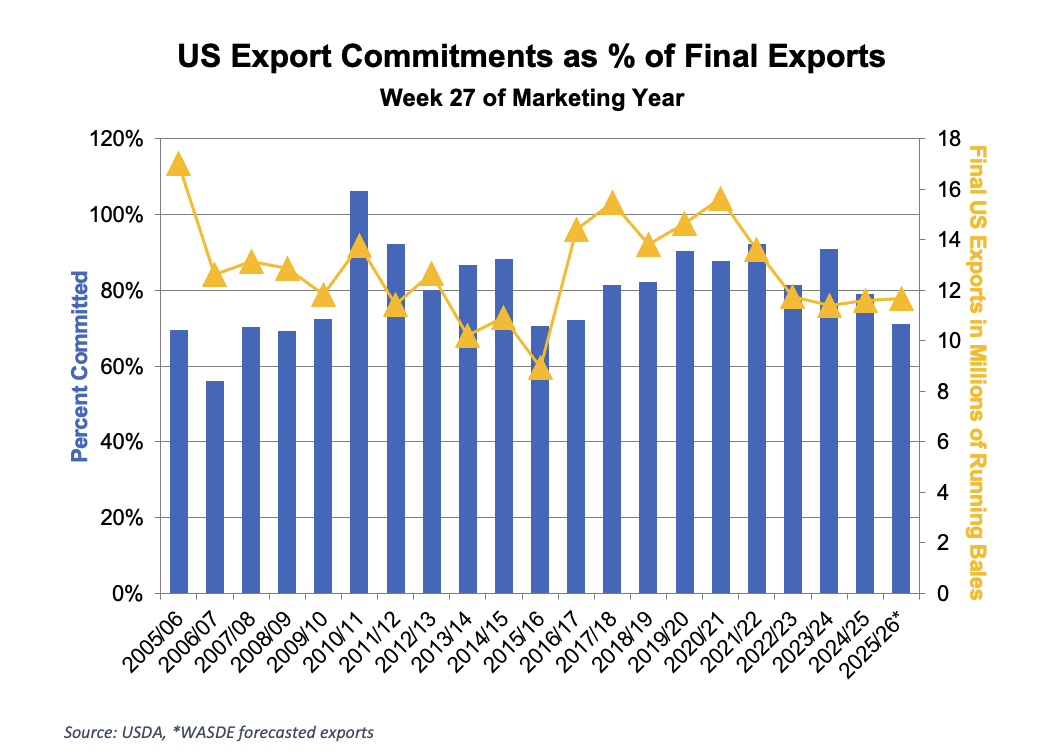

- The USDA Outlook Forum on Thursday will release the first model-based 2026/27 balance sheets. While these numbers are not survey-driven, they will serve as an early framework for next year’s acreage and demand assumptions. With margins still tight and policy uncertainty lingering, the market will scrutinize these tables for clues on planted area and use expectations.

- Macro direction still matters. A firm Chinese yuan and a weaker U.S. dollar are supportive on the margins, but if risk sentiment deteriorates further, cotton could feel spillover pressure from equities and broader commodity flows.

- The Zhengzhou Commodity Exchange, where Chinese cotton futures trade, will remain closed through February 24 for the Lunar New Year holiday. Business out of China will likely be quieter during that period.

Overall, the week offers more tone-setting catalysts than outright balance-sheet changes. Cotton is not facing a dramatic shift in fundamentals at the moment, but the intersection of macro signals, early acreage expectations, and positioning will likely determine whether prices stabilize, grind sideways, or attempt to build modest momentum.

Market Recap

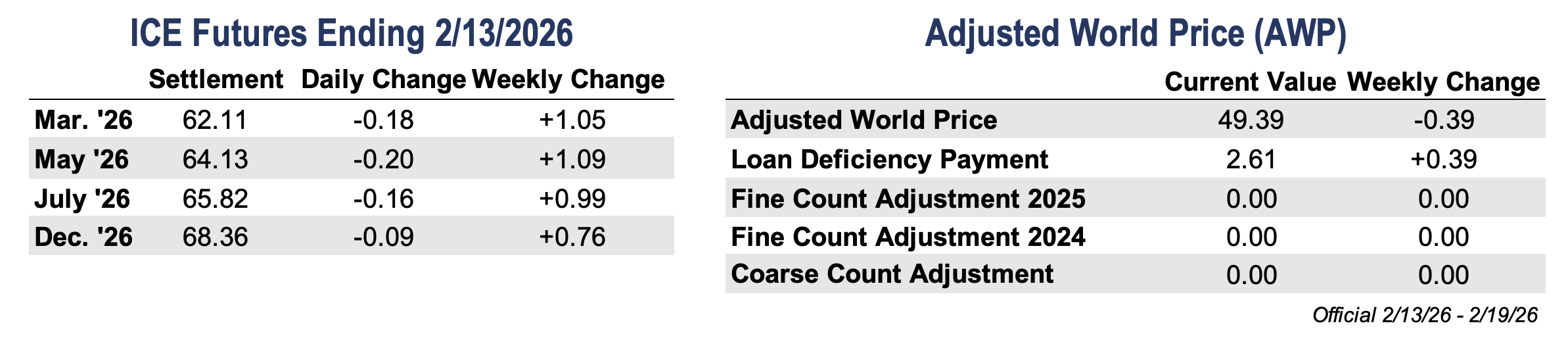

- March and May futures finished the week modestly higher following an active stretch of trading. The March contract gained 105 points to settle at 62.11 cents per pound on Friday, while May rose 109 points on the week to close at 64.13 cents.

- Trading activity was elevated throughout the week, driven largely by index roll flows and continued March liquidation ahead of First Notice Day. ICE posted some of the highest volumes on record, with spreads accounting for much of the activity as open interest declined and positions rolled forward. Despite volatility and weakness in nearby spreads, both contracts held onto weekly gains.

- Certified stocks continued to build, adding pressure to the front spreads, with March and May briefly trading to new contract lows before stabilizing. Speculators also extended their net short position, keeping downside pressure in place even as prices edged higher. Supportive headlines surrounding the U.S.–Bangladesh trade agreement and improving U.S.–China dialogue offered some optimism, but overall, the market spent the week digesting positioning, flows, and early acreage expectations rather than establishing a clear new trend.

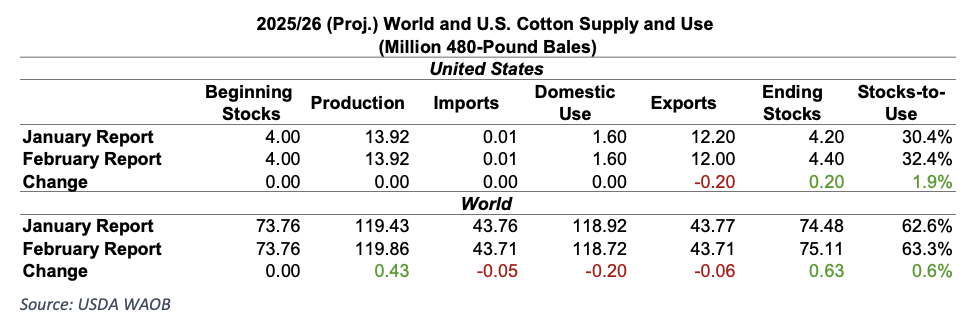

- The National Cotton Council projected 2026 U.S. cotton acreage at 8.99 million acres, down 3.2 percent year over year. The largest expected decline in Upland acres came from the Midsouth, down 20.6 percent to 1.19 million acres. The Southeast is projected at 1.63 million acres, down 4.9 percent, while the Far West is expected at 125,000 acres, down 7.2 percent. The Southwest is the only region showing an increase, projected up 1.6 percent to 5.88 million acres. Using survey assumptions, total production across the Cotton Belt is projected at 12.74 million bales, with lower ending stocks anticipated for 2025/26 and 2026/27. As one of the first planting surveys of the season, the report provides an early directional signal of producer intent heading into spring.

- Trading volumes were heavy throughout the week, with strong activity across the board. Open interest decreased by 31,613 contracts to 344,646. Meanwhile, certificated stocks continued to build, rising 12,479 bales to 106,040 bales.

The Seam®

The Seam®