The macro backdrop will take center stage this week, with several key events likely to shape overall market direction.

The Federal Reserve meets Wednesday, and while a rate hold is widely expected, the focus will be on tone. With inflation still running firm, any shift in language around policy direction or timing could move markets.

Thursday brings a full slate of data, including first-quarter GDP along with personal income and PCE inflation – the Fed’s preferred measure of inflation. Growth is expected to come in steadily, but markets will be paying closer attention to underlying strength in the consumer and whether inflation shows signs of easing.

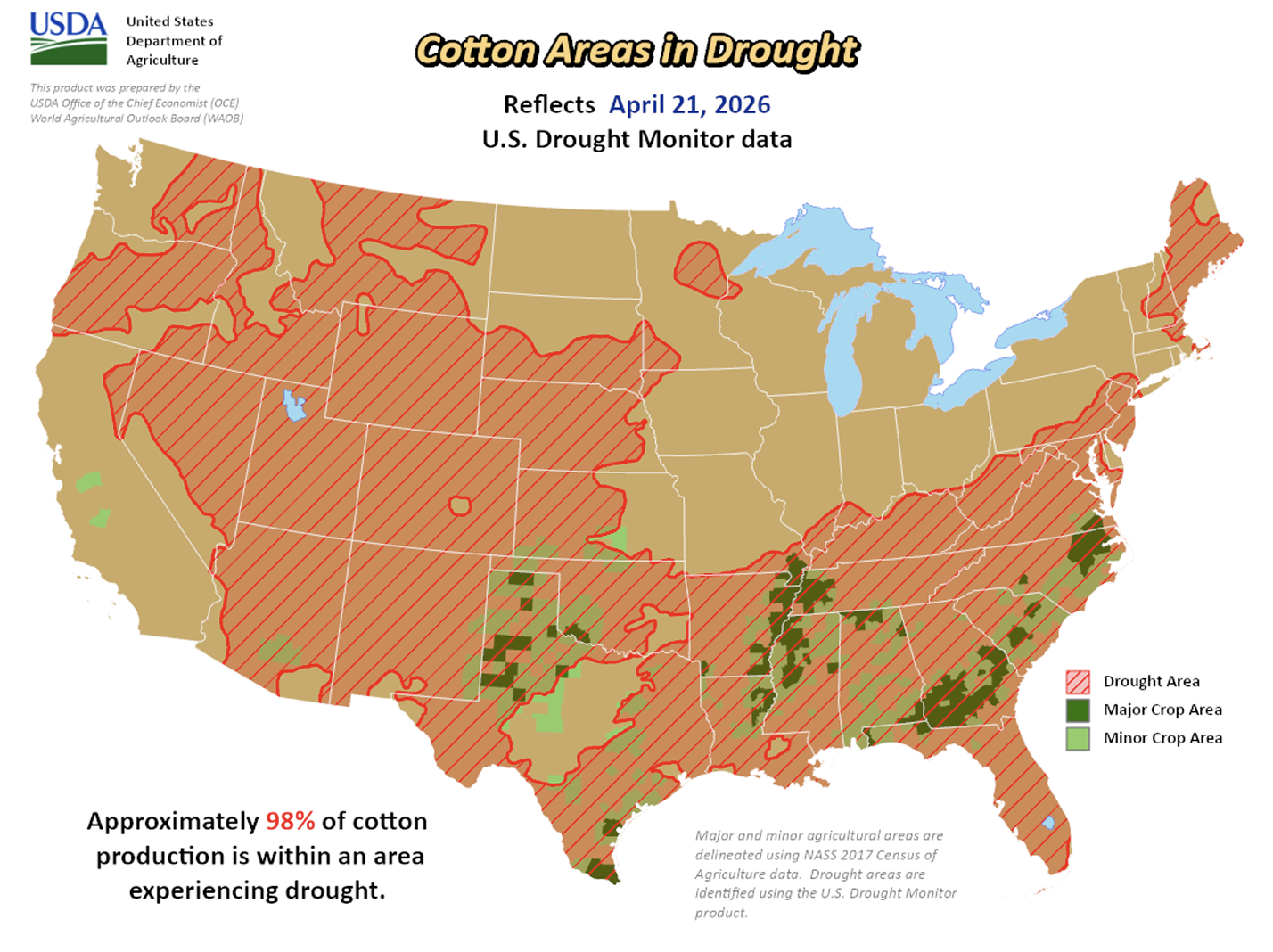

For cotton, macro will continue to lead. Energy and broader market sentiment remain closely tied to price direction, while on the fundamental side, drought remains a concern with nearly the entire Cotton Belt still experiencing some level of dryness as planting progresses.

Market Recap

Cotton futures had a choppy week, with July trading near recent highs before pulling back midweek and stabilizing into the end of the period. July futures settled at 79.36 cents per pound, down a modest 46 points on the week, while May closed at 77.00 cents on First Notice Day.

New crop strength remained a theme, with December pushing to a new contract high before easing. Despite the midweek correction, prices remain elevated, marking one of the stronger stretches in recent trading.

Price action was driven by a combination of macro headlines, technical positioning, and ongoing trade activity. Early last week, geopolitical tensions surrounding Iran and the closure of the Strait of Hormuz supported crude oil and lent spillover strength to cotton. That momentum faded midweek as overbought conditions caught up with the market, prompting a sharp correction with no clear headline trigger. By late week, prices found support and rebounded, and an overall bullish sentiment remains in the market.

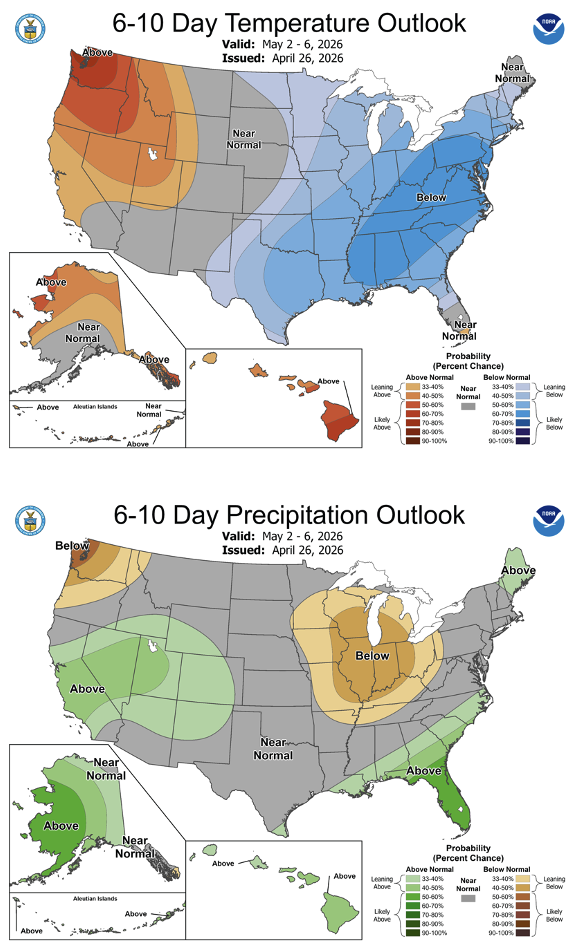

On the fundamental side, drought conditions remain a key underlying factor. The latest U.S. Drought Monitor showed 98% of U.S. cotton areas experiencing some level of drought, up from 97% the prior week and significantly higher than this time last year. Within that, a large portion of the Cotton Belt is facing severe to exceptional conditions. While some rainfall is forecast over the week, conditions across much of the Cotton Belt remain tight as planting progresses, keeping weather risk firmly in focus.

Trading activity remained elevated across futures, options, and spreads, with managed money a net buyer for the seventh consecutive week. On-call activity stayed active through May liquidation. Open interest declined as May approached First Notice Day amid broader liquidation, while certificated stocks increased 714 bales to 165,681.

Economic and Policy Outlook

Over the weekend, tensions with Iran escalated, with the U.S. signaling a shift toward remote negotiations while activity around the Strait of Hormuz intensified, including vessel boardings and increased enforcement. A ceasefire in the region was extended, though broader uncertainty remains. Iran has floated reopening the Strait with conditions, adding further risk to global shipping and energy flows. This follows a volatile week driven by similar headlines, with crude oil moving higher as macro risk continues to steer markets.

Secretary of Agriculture Brooke Rollins’ appearance before Senate appropriators last week was largely focused on the FY27 USDA budget, but her remarks took an unexpected turn toward policy, with notable support for the Buying American Cotton Act (BACA). While the hearing centered on proposed funding cuts and restructuring, Rollins emphasized BACA as a priority, calling it a “game changer” for cotton producers and stating she “wants to do whatever I can to support it,” highlighting its alignment with broader administration initiatives.

USDA increased Supplemental Disaster Relief Program (SDRP) payments from 35% to 70% for approved 2023 and 2024 disaster losses, providing an additional 35% top-up to prior payments and setting future payouts at 70%. The application deadline was extended to August 12, 2026, giving producers more time to update or finalize submissions. To date, $6.7 billion has been distributed through SDRP, part of a broader push to strengthen the farm safety net amid ongoing economic and weather-related pressures.

The House is expected to vote on the Farm Bill later this week, though the path forward remains uncertain as leadership works through amendment decisions and procedural hurdles.

Supply and Demand Overview

U.S. export sales softened in the most recent report, with net upland sales totaling 119,900 bales for the current marketing year, down from the previous week and well below the recent pace. Vietnam, Turkey, and Pakistan continued to lead buying, with additional support from India and Malaysia, while some cancellations from China weighed on totals. New crop sales picked up to 57,100 bales, led by Vietnam and Indonesia. Pima sales were a bright spot, reaching a marketing-year high of 36,200 bales, driven primarily by India and China.

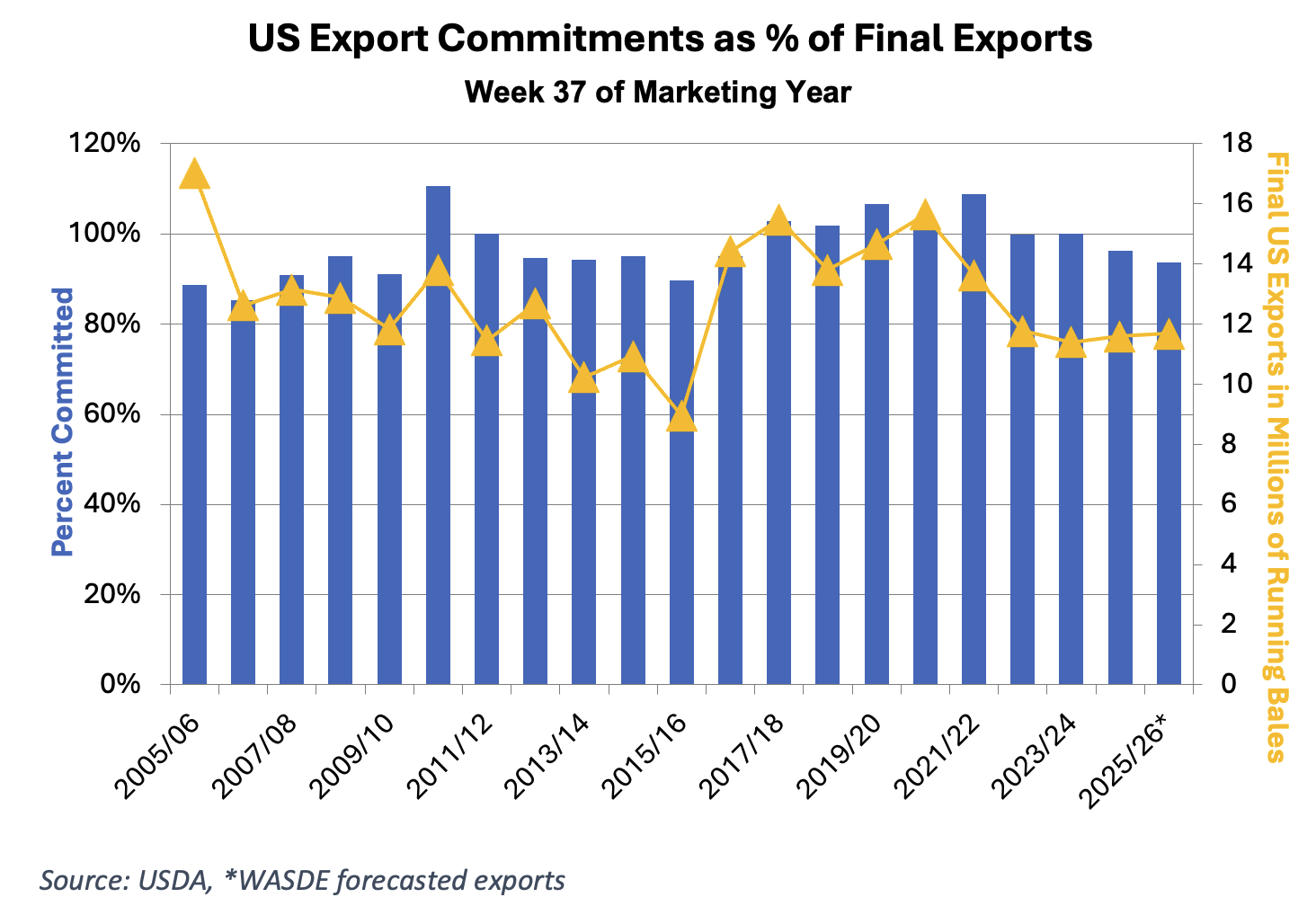

Shipments came in at 296,400 bales, slightly below the prior week and recent average but still near the pace needed to stay on track for USDA’s 12 million bale export target if maintained. Pima shipments were lighter at 4,500 bales, though overall demand remains supportive. As peak shipping season continues, exports are holding together, but will still need to average just under 295,000 bales per week to meet the target.

The Seam®

As of Friday afternoon, grower offers totaled 15,922 bales. The past week, 1,203 bales traded on the G2B platform received an average price of 70.15 cents per pound. The average loan redemption rate (LRR) was 52.46, bringing the average premium over the LRR to 17.69 cents per pound.

Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).

Sustainability Enrollment Opportunities

Reminder, enrollment for the U.S. Cotton Trust Protocol ends this Thursday, April 30, 2026. Growers who are currently enrolled will need to renew their membership to continue their involvement in the program. If your gin would like to host an Enrollment Field Day during this time, please reach out to PCCA at (806) 763-8011. Click here for a list of in-person sign-up dates.

New Grower Enrollment for the Better Cotton Initiative will be open from March 3 to May 30. Growers interested in joining this global sustainability program should contact PCCA (806) 763-8011.

Latest News

U.S. EXPORT SALES

For Week Ending 18-Jun-2026

2025-2026

Net Upland Sales 83,864

Upland Shipments 3,00,155

Net

Sustainability Enrollment Opportunities

Sustainability Enrollment Opportunities