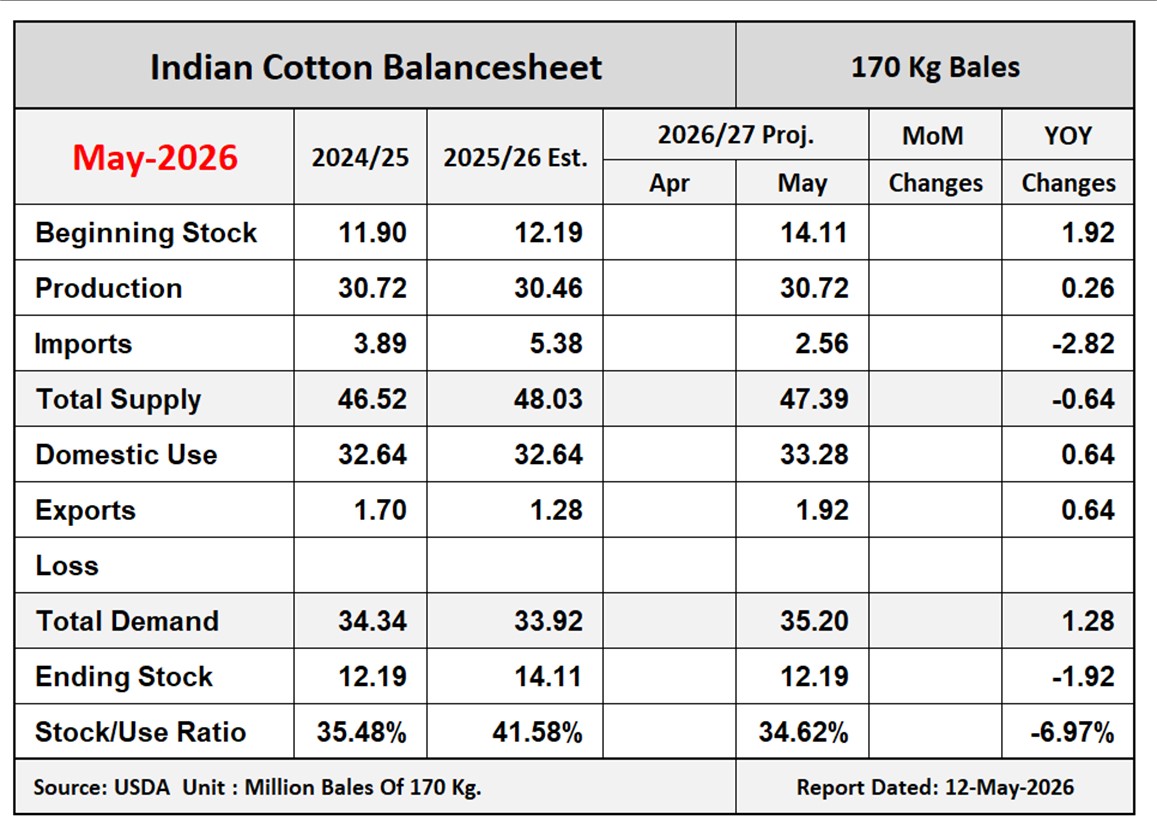

USDA-WASDE

May-2026

COTTON: The first forecast of the 2026/27 U.S. cotton balance sheet shows lower production and ending stocks, and higher exports and beginning stocks compared to 2025/26, with consumption unchanged. Planted area is projected at 9.64 million acres based on the March 31 Prospective Plantings report. Harvested area is forecast to be 7.38 million acres for an abandonment rate of about 24 percent, approximately equal to the 10-year average. The 2026/27 national average yield is projected at 866 pounds per harvested acre based on regionally weighted 5-year averages, slightly above last year’s 852 pounds. Production is projected to be 13.30 million bales, 600,000 below the 13.90 million bales produced in 2025/26. Exports are projected 300,000 bales higher at 12.30 million due to higher global demand and stocks are drawn down. As a result, ending stocks are forecast to be 500,000 bales lower at 3.90 million, for an ending stocks-to-use ratio of 28.1 percent. The projected season-average price for 2026/27 is 73 cents per pound.

U.S. all-cotton production for 2025/26 is lowered 21,000 bales to 13.90 million. There are no other changes to supply and demand categories in the 2025/26 U.S. cotton balance sheet this month. The season-average farm price forecast is raised 2 cents to 63 cents per pound reflecting recent strength in cotton futures.

World supply for 2026/27 is down 2 percent from 2025/26 as global production is projected 6.6 million bales lower, more than offsetting the 2.8-million-bale increase in beginning stocks. World consumption is projected to increase 1 percent to 121.7 million bales led by increases for China, India, Bangladesh, Egypt, Pakistan, and Vietnam (up collectively 1.5 million bales). Global trade is expected to be 1 percent lower at 43.4 million bales as reduced imports by India more than offset increases for Pakistan, China, Vietnam, and other countries. Ending stocks are down 7 percent from 2025/26 at 71.8 million bales as Australia, Brazil and the United States draw down stocks to support exports given smaller crops, and India and China draw down stocks to support consumption.

The 2025/26 world balance sheet is revised to show higher production, consumption, and beginning and ending stocks, with trade marginally increased. The global production estimate is raised nearly 1 percent to 122.6 million bales as an almost 900,000-bale increase for Uzbekistan is partially offset by a reduction for Argentina. Consumption is increased by almost 1 percent as mill use in Uzbekistan is raised 1 million bales, reflecting its much larger crop, and consumption in China is revised 500,000 bales higher. Partially offsetting reductions are expected for Pakistan and Vietnam, with small adjustments for several countries. Ending stocks are forecast to increase by around 220,000 bales as the increases in beginning stocks and production exceed that for consumption. The ending stocks-touse ratio is down slightly to 64.3 percent.