PCCA Cotton Market Weekly 01-Aug-2025

Posted : August 02, 2025

August 1, 2025

Cotton prices moved lower this week, as soft demand, tariff uncertainty, and broader market pressure kept futures on the defensive. With the new crop year underway and macro risks still swirling, will cotton find fresh direction or stay stuck in the summer slump? Get QuickTake’s read on the week’s events in five minutes.

Cotton prices drifted lower this week, with pressure from weak demand, ongoing trade uncertainty, and broader market headwinds keeping futures in check.

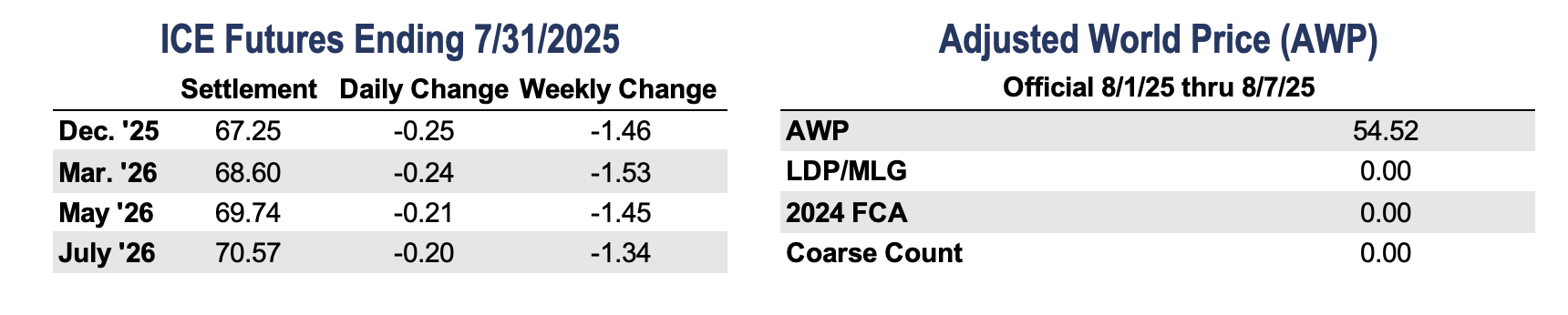

- December futures ended the week at 67.25 cents per pound, down 146 points from the previous week.

- Cotton prices drifted lower this week, weighed down by continued weak demand for textiles and ongoing tariff uncertainty. The August 1 tariff deadline kept traders on edge, and the announcement of new tariffs pressured prices further. December futures fell below key technical levels, triggering additional selling. The latest On-Call report showed a widening gap between unfixed purchases and sales, reflecting continued grower pricing and limited mill participation. With the 2024/25 marketing year now complete as of July 31, attention shifts to the new crop year as the market looks for direction on supply and demand.

- The Adjusted World Price (AWP) calculation will use new crop quotes and the 2025 sum of adjustments, which will apply starting the week of August 8.

- Trading volume picked up this week, and open interest rose by 4,241 contracts to 224,510. Certificated stocks edged down by 18 bales to 21,617, the lowest level since early May.

Tariff tensions returned to the spotlight this week as the August 1 deadline arrived, contributing to mixed market performance amid a wave of economic data.

- President Trump signed an executive order establishing a new baseline tariff regime affecting over 70 countries, set to take effect on August 7. While most nations will face a 10% tariff, many key importers of U.S. cotton were assigned higher rates. The order also includes a 40% tariff on transshipped goods — items rerouted through third countries to bypass higher duties. Notable actions include a 90-day extension of the trade deal with Mexico, a 35% tariff imposed on Canada, and a surprise 25% tariff levied on India.

- New inflation data shows prices remain above the Fed’s 2% target, with the Personal Consumption Expenditures (PCE) index, the Fed’s preferred inflation gauge, rising 2.6% in June. Core PCE, which strips out volatile food and energy prices, rose 2.8%, with prior months also revised higher. Tariffs are driving broader price increases and weighing on consumer spending, adding to the economic strain amid rising costs and trade uncertainty.

- July’s jobs report missed expectations, with payrolls up just 73,000 and major downward revisions to the prior two months cutting 258,000 jobs. This shift is raising concerns about the actual strength of the labor market. The unemployment rate ticked up to 4.2%, and the three-month average gain now sits at just 35,000. The Fed held rates steady this week with a hawkish tone, but following Friday’s numbers, markets are now pricing in a greater chance of a rate cut in September.

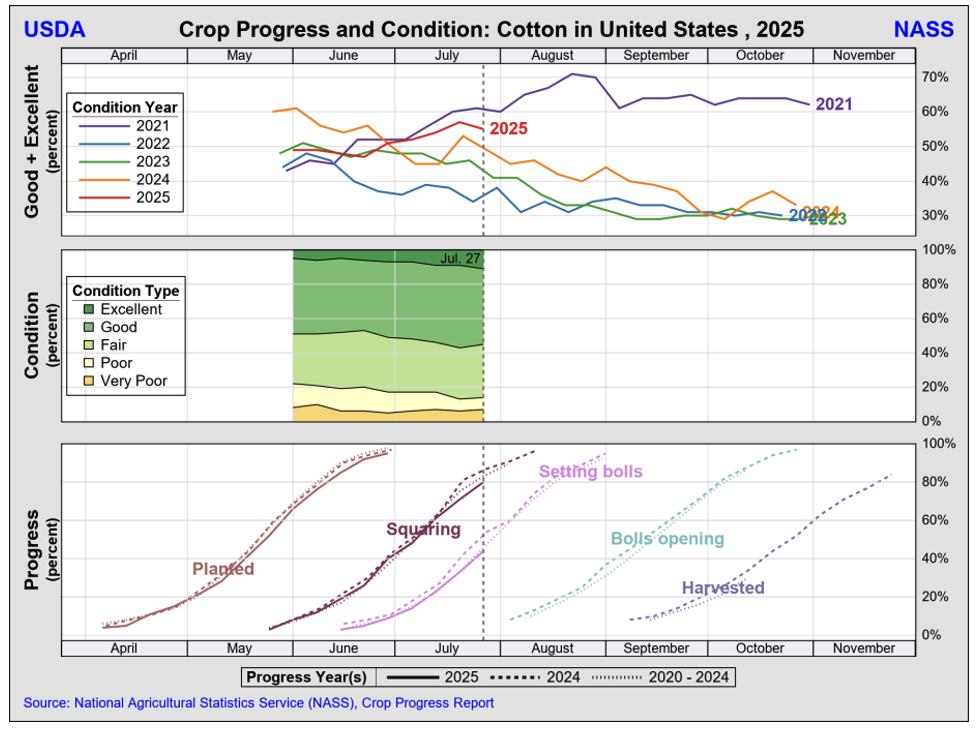

Crop development in the Southwest continues, though progress varies by region. Conditions have softened, with the season’s first weekly decline now reported.

- As of July 28, crop condition ratings declined slightly in Texas and Oklahoma, with 50% and 53% rated good to excellent, respectively. Kansas held steady at 52% good to excellent.

- Squaring and boll development continue, though progress remains mixed. The consensus is that a decent portion of the crop is behind this year. Texas reports 75% of its crop squaring and 40% setting bolls. Oklahoma is at 77% squaring and 15% setting bolls, while Kansas leads with 85% squaring and 27% setting bolls.

- Scattered storms brought some relief to parts of West Texas and southwestern Oklahoma, though most areas remain dry. A brief break from extreme heat helped fruiting plants, but hot conditions are expected to return. Weed pressure persists where rainfall was spotty. In South Texas, harvest is progressing under hot, dry weather, with defoliation and picking underway. Forecasts call for continued warmth and limited rain, allowing fieldwork to move forward with few interruptions.

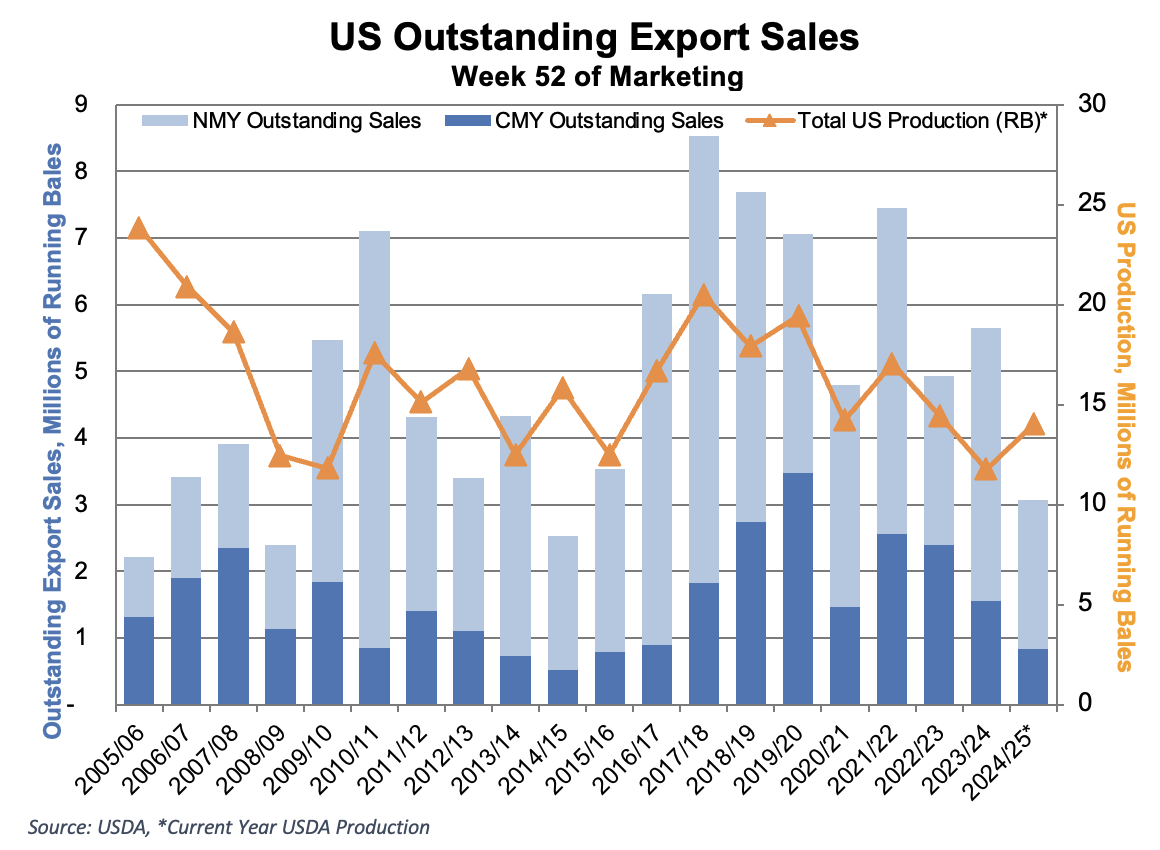

Export shipments remain strong as new crop sales lag and carryover hits multi-year lows.

- U.S. export sales remained modest this week, with net sales for the 2024/25 crop year totaling 39,100 bales, staying above the 4-week average. As expected this late in the season, most buyers shifted to new crop, with net 2025/26 sales reaching 71,700 bales. Vietnam led current and new crop sales, followed by Honduras, Pakistan, and Turkey.

- Shipments were strong again at 239,600 bales, leaving the U.S. just 57,000 bales short of USDA’s 11.8 million bale export estimate, which could be raised in the upcoming supply and demand estimates. With just one report remaining, traders are noting the U.S. is on track for the smallest sales carryover since 2016/17 and the lowest new crop commitments since 2014/15.

- Pima sales were minimal, with just 100 bales sold for the current year and 5,000 for new crop. Exports totaled 8,700 bales, led by shipments to India, China, and Pakistan.

The Week Ahead

- With July behind us and the new crop year underway, data releases are expected to slow next week. Aside from the usual cotton reports, attention will turn to headlines for clues on what might move markets.

The Seam

The Seam

As of Thursday afternoon, grower offers totaled 24,422 bales. There were 957 bales that traded on the G2B platform that received an average price of 61.88 cents per pound. The average loan for these bales was 52.39, bringing the average premium received to 9.49 cents per pound.