PCCA Cotton Market Weekly 16-Mar-2026

Posted : June 25, 2026

March 16, 2026

The Week Ahead

Markets will be closely watching developments in the Middle East this week, with attention also turning to Wednesday’s Federal Reserve policy decision.

- Geopolitical developments will remain in focus, particularly the situation in the Middle East and any disruptions to global energy flows. In addition, U.S and China trade discussions beginning this week will be watched for any signals around potential agricultural purchases. Crude oil remains the dominant influence across markets. At one point, prices pushed above $100 per barrel as the war involving Iran and disruptions to shipping through the Strait of Hormuz heightened concerns about global supply.

- Attention this week will also largely center on the Federal Reserve. Wednesday’s policy decision and press conference from Chair Powell will be closely watched as markets evaluate how the recent surge in energy prices may influence the outlook for inflation and interest rates. Higher oil prices could push inflation expectations higher, which could complicate the Fed’s path toward easing policy later this year.

Overall, macro developments continue to set the tone across commodity markets, with energy prices and fund flows currently driving sentiment more than underlying agricultural fundamentals. Looking ahead, market attention is beginning to shift toward upcoming USDA reports, including the Prospective Plantings report later this month.

Market Recap

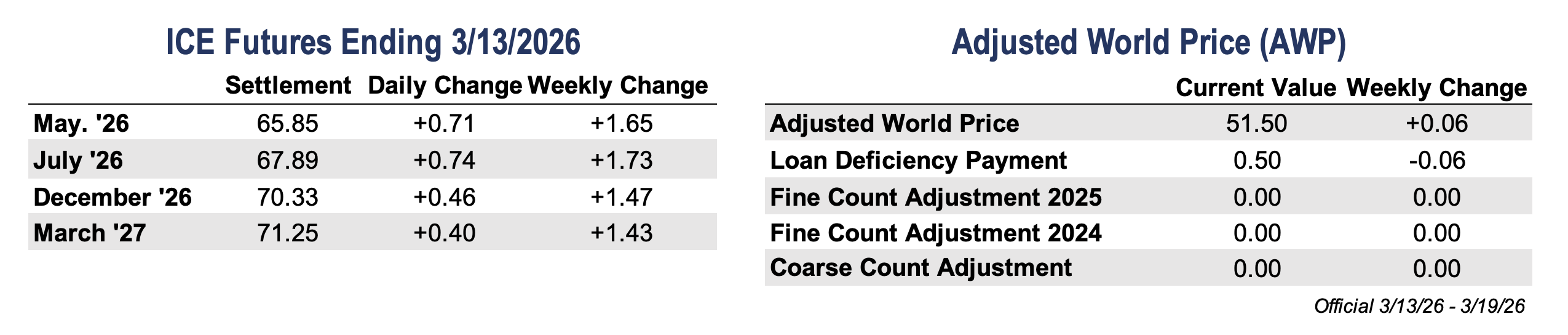

- Cotton futures posted modest gains this week as markets navigated continued volatility across the broader macro landscape. May futures finished the week 165 points higher, settling at 65.85 cents per pound, after trading in a relatively narrow range compared to the large swings seen in energy and financial markets.

- Much of last week’s attention remained focused on developments surrounding the ongoing conflict in the Middle East. Energy markets experienced significant volatility, with crude oil briefly pushing toward $120 per barrel before retreating back below $100 as headlines shifted throughout the week. While sharp moves in crude oil and other markets created broader uncertainty across the commodity complex, cotton prices were comparatively steady and avoided the large swings seen elsewhere.

- Cotton did find some technical support late in the week, with May futures closing above the 100-day moving average for the first time since late February. News that China approved an additional 300,000 metric tons of sliding scale import quotas helped keep buyers engaged, as the spread between domestic and international prices has widened.

- On-call activity also continued to show gradual improvement. The latest CFTC Cotton On-Call report indicated unfixed sales increased while unfixed purchases declined, further narrowing the imbalance between the two and continuing the trend seen over the past several weeks.

- Trading activity stayed strong throughout the week, with solid participation across the board. Open interest increased by 8,039 contracts to 334,317, while 12,513 bales were decertified, making certificated stocks at 116,789 bales.

Economic and Policy Outlook

Economic and Policy Outlook

- Markets spent much of last week focused on developments surrounding the Strait of Hormuz as tensions tied to the Iran conflict continued to disrupt energy markets and global trade flows. Tensions escalated further over the weekend, with threats to Iran’s Kharg Island export terminal adding to concerns about global oil supply. The broader backdrop remains complicated as the conflict comes on top of existing trade tensions tied to ongoing tariff policies, adding another layer of uncertainty for global markets.

- Uncertainty surrounding U.S. and China relations increased last week after President Trump suggested a planned summit with Chinese President Xi Jinping could be delayed. The meeting had been expected to follow several weeks of diplomatic groundwork aimed at stabilizing relations and advancing potential economic agreements. However, Trump indicated the timing of the summit could depend on China’s willingness to help address disruptions in the Strait of Hormuz tied to the Middle East conflict. While officials from both countries continue discussions on trade and economic cooperation, the possibility of a delay adds another layer of uncertainty to an already fragile diplomatic reset.

- Attention also turned to a busy slate of central bank meetings, including the Federal Reserve, as policymakers weigh the impact of higher energy prices alongside signs of slowing economic growth. Last week’s inflation data showed U.S. CPI rose 0.3% month over month in February, in line with expectations, while the annual rate held steady at 2.4%. Meanwhile, data also showed consumer spending increased modestly in January while core inflation remained elevated, with prices excluding food and energy up 3.1% from a year ago. At the same time, some indicators suggest economic momentum may be cooling. The added pressure from higher energy prices tied to the Iran conflict has further complicated the outlook and could keep the Fed cautious on interest rate cuts for now.

Supply and Demand Overview

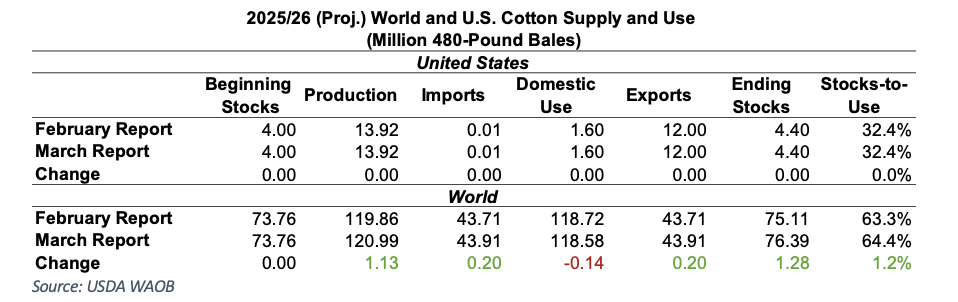

- USDA’s March WASDE report was released on Tuesday of last week, but had little impact on the cotton market. U.S. balance sheet estimates were left unchanged, while global ending stocks increased slightly as higher production from Brazil and China more than offset small adjustments elsewhere, and consumption was lowered in several countries. Overall, the report was largely neutral, though if anything, it leaned slightly bearish given the increase in global stocks and softer consumption. Traders quickly moved past the report and shifted their focus toward the upcoming Prospective Plantings report at the end of the month.

- Export sales improved from the previous week. Net Upland sales totaled 253,200 bales, with an additional 36,600 bales booked for next marketing year. Vietnam led the way in purchases, followed by Bangladesh, Pakistan, India, and Indonesia. Shipments strengthened considerably, reaching a marketing-year high of 370,100 Upland bales along with 17,900 Pima bales. This week’s shipments came in well above the roughly 300,000 bales needed each week for the U.S. to reach USDA’s 12 million bale export projection, providing a supportive signal for demand.

The Seam®

The Seam®

- As of Friday afternoon, grower offers totaled 36,891 bales. The past week, 15,604 bales traded on the G2B platform received an average price of 58.40 cents per pound. The average loan redemption rate (LRR) was 50.15, bringing the average premium over the LRR to 8.25 cents per pound.

Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).

Sustainability Enrollment Opportunities

- Enrollment for the U.S. Cotton Trust Protocol will be open January 5th- April 30th, 2026. Growers who are currently enrolled will need to renew their membership to continue their involvement in the program. If your gin would like to host an Enrollment Field Day during this time, please reach out to PCCA at (806) 763-8011. Click here for a list of in-person sign-up dates.

- New Grower Enrollment for the Better Cotton Initiative will be open from March 3 to May 30. Growers interested in joining this global sustainability program should contact PCCA (806) 763-8011.