PCCA Cotton Market Weekly 04-May-2026

Posted : June 25, 2026

May 4, 2026

The Week Ahead

Macro will stay in the driver’s seat this week, with several moving pieces likely to influence overall direction.

- Friday’s jobs report is the main event. Expectations are fairly neutral, so the reaction will matter more than the number itself. The dollar will be key to watch – strength there would likely lean against export-heavy commodities like cotton, while any weakness could be supportive.

- It’s a full week otherwise, with labor data scattered throughout and a heavy round of earnings tied to the ag space. Markets are still holding together well, with outside support coming from equities and a generally firm inflation picture.

- For cotton, macro is still doing most of the heavy lifting. Energy and broader market direction remain closely tied to price movement, and higher crude oil prices are starting to matter more – raising polyester costs and, at the margin, improving cotton’s competitiveness.

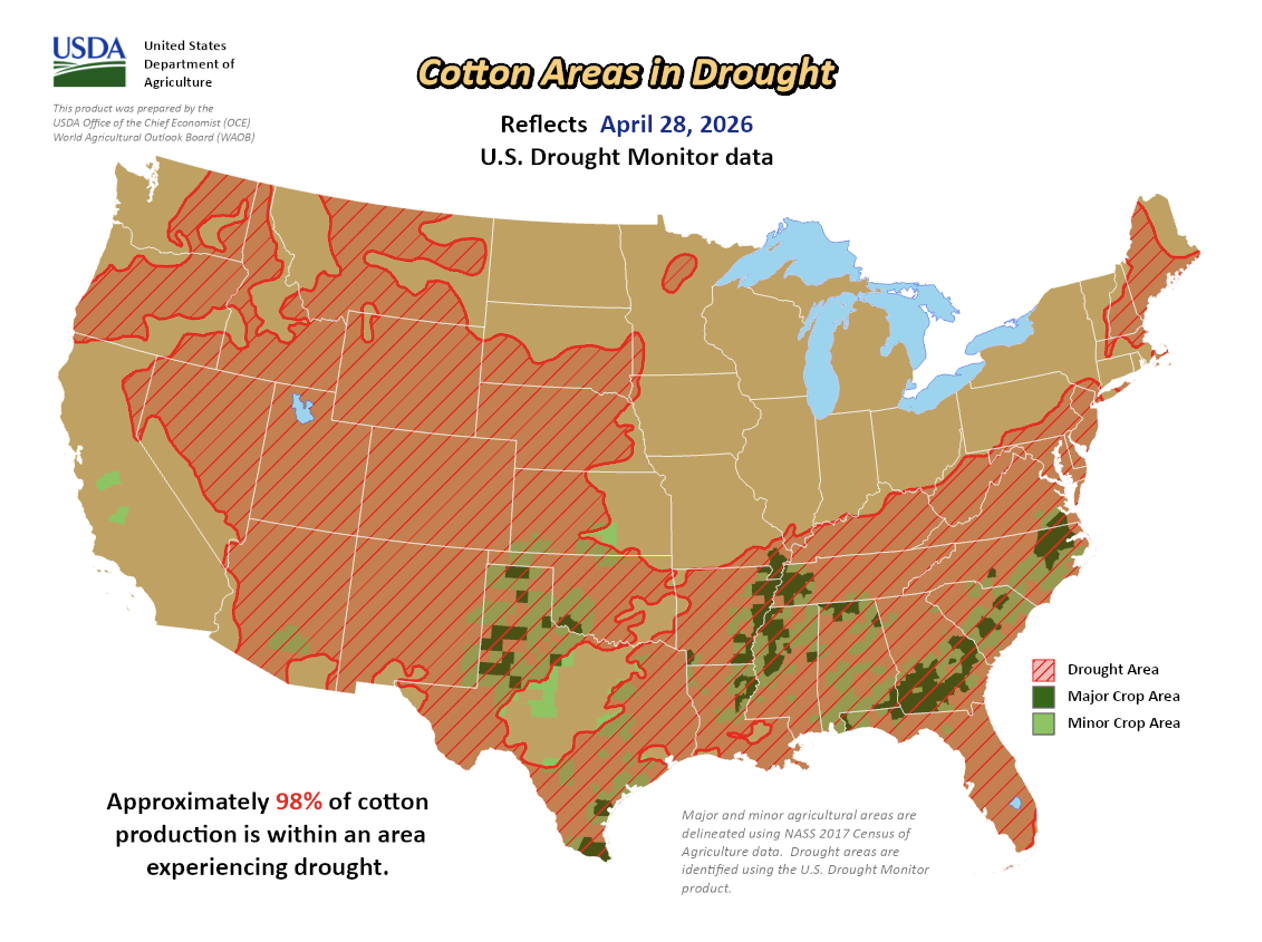

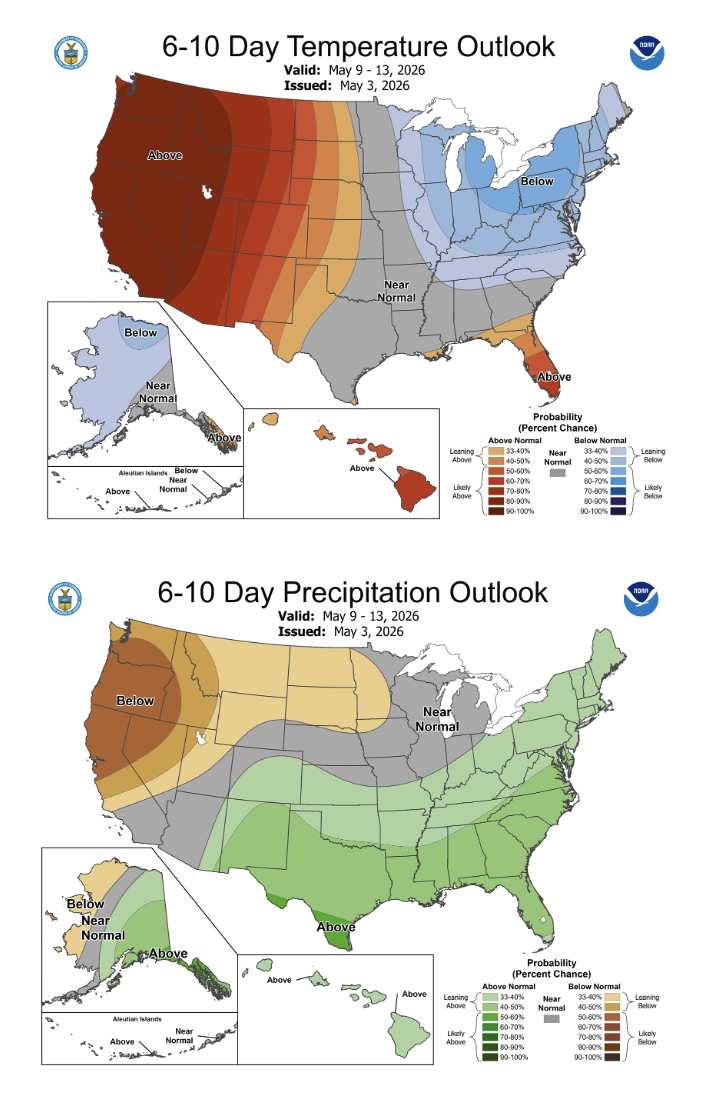

- At the same time, the market is beginning to lean more into weather than it has in recent weeks. Planting delays are offering some near-term support, while dryness across key areas in the Cotton Belt continues to hang over the outlook, though any meaningful shift toward moisture could quickly add pressure to prices.

- Next week’s supply and demand update will give the first look at the 2026 balance sheet, including how weather is being factored in and where global consumption stands.

Market Recap

- Cotton futures moved higher last week, with July extending the rally and settling at 84.19 cents per pound, up roughly 483 points. December followed, closing at 84.56 and continuing to hold strength in new crop. Prices are now sitting near some of the highest levels since mid-2024.

- After a quiet start to the week, prices reacted to positive fundamental signals. Strong export sales and shipments, along with continued mill buying and speculative interest, pushed futures sharply higher. The move included a limit-up session that pushed prices to new contract highs. Typically, that kind of move can signal the market is becoming overbought, but the market held together into the end of the week. There was also talk of a potential Chinese reserve release surfacing overnight on Thursday, which likely contributed to some of the early volatility. Outside markets added support at times, particularly through crude oil tied to ongoing Iran developments, though intraday volatility picked up as shifting weather expectations.

- On the fundamental side, weather is starting to matter more. Recent rainfall across parts of the Mid-South and Southeast provided some relief, with additional moisture in the forecast, including West Texas. While that supports crop conditions, it can also weigh on prices if realized. Even so, drought remains widespread across the Cotton Belt, keeping production risk in focus as planting progresses.

- Trading activity was lighter early in the week before picking up alongside the rally, with a noticeable increase in options volume. Managed money remained a net buyer, extending the recent trend, while on-call data showed a widening imbalance driven by more unfixed purchases. Open interest has been fluid around the May delivery period, while certificated stocks posted an increase on the week.

Economic and Policy Outlook

- Tensions around the Strait of Hormuz picked up again, with the U.S. stepping in to help move commercial ships while Iran continues to push back on access. The back-and-forth has kept uncertainty high, with no clear path to resolution and control of the waterway still in question. That’s continued to drive volatility, particularly in crude oil, with sharp reactions to headlines spilling over into broader commodity markets, including cotton.

- A new version of the farm bill cleared the House this week, but on a tight, mostly party-line vote. Much of the debate centered around amendments, particularly on pesticide policy and nutrition programs, with some of the more contentious provisions being removed along the way. From here, attention shifts to the Senate, where the bill will continue to take shape. Of course, the big-ticket Farm Bill items like the ARC/PLC programs and the Marketing Assistance Loan were in the One Big Beautiful Bill Act from last summer.

- Separately, lawmakers advanced a key budget framework after some internal delays, allowing work to move forward on funding priorities and avoiding any immediate shutdown risk. While there are still a number of unresolved issues across DHS funding and other legislation, the government remains open for now. Ag was unaffected because it received a full year of funding in the fall.

- The Fed held rates steady last week, but the tone leaned more hawkish, with a few officials already pushing back on signaling future cuts and the broader committee drifting closer to neutral. Markets reacted by pulling back rate cut expectations, with yields moving higher and the dollar firming. On the data side, GDP came in a bit lighter at +2.0% versus expectations, while inflation held steady with PCE at +0.7% month-over-month, and consumer strength showed through with income up +0.6% and spending up +0.9%, keeping the macro picture supportive but a bit more mixed.

Supply and Demand Overview

- U.S. export sales improved in the most recent report, with net upland sales totaling 162,900 bales for the current marketing year, up from the previous week. Vietnam and Pakistan led the way again, with additional support from Honduras, Bangladesh, and India, while some cancellations from China weighed on totals. New crop sales were stronger at 105,700 bales, led primarily by Turkey and China.

- Shipments picked up significantly, coming in at 384,600 bales, up both week-over-week and from the recent average. Vietnam remained the top destination, followed by Pakistan, Turkey, and India. Pima sales eased to 21,900 bales but remain steady overall, while shipments were strong at 17,800 bales. As peak shipping season continues, exports are holding together well and running ahead of the pace needed to reach USDA’s 12 million bale target if sustained.

The Seam®

- As of Friday afternoon, grower offers totaled 14,592 bales. The past week 3,915 bales traded on the G2B platform received an average price of 76.36 cents per pound. The average loan redemption rate (LRR) was 53.73, bringing the average premium over the LRR to 22.63 cents per pound.

Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).

Sustainability Enrollment Opportunities

- New Grower Enrollment for the Better Cotton Initiative will be open from March 3 to May 30. Growers interested in joining this global sustainability program should contact PCCA (806) 763-8011.